Financial Markets

本文是学习 https://www.coursera.org/learn/financial-markets-global这门课的学习笔记

这门课的老师是耶鲁大学的Robert Shiller https://en.wikipedia.org/wiki/Robert_J._Shiller

Robert James Shiller (born March 29, 1946)[4] is an American economist, academic, and author. As of 2022,[5] he served as a Sterling Professor of Economics at Yale University and is a fellow at the Yale School of Management’s International Center for Finance.[6] Shiller has been a research associate of the National Bureau of Economic Research (NBER) since 1980, was vice president of the American Economic Association in 2005, its president-elect for 2016, and president of the Eastern Economic Association for 2006–2007.[7] He is also the co‑founder and chief economist of the investment management firm MacroMarkets LLC.

Week 02

In this next module, dive into some details of behavioral finance, forecasting, pricing, debt, and inflation.

Learning Objectives

- Understand the concept of limited liability and its connections with psychology, risk diversification and corporate finance.

- Describe inflation indexed debt, and monetary innovation designed to tackle hyperinflation.

- Understand the basics of the real estate market, assumptions behind forecasting the stock market, and the basic framework to price a stock.

- Describe the key intuition and definitions behind the Efficient Market Hypothesis, and why it might only be half-truth.

- Understand the basics of the real estate market, assumptions behind forecasting the stock market, and the basic framework to price a stock.

- Describe the key intuition and definitions behind the Efficient Market Hypothesis, and why it might only be half-truth.

- To describe and provide examples of the wishful thinking bias and of cognitive dissonance.

- List the key features of Antisocial Personality Disorder and Borderline Personality Disorder.

文章目录

以下是几个常见的与“economic”相关的单词以及它们的音标:

Economic

- 英式发音: /ˌiː.kəˈnɒm.ɪk/

- 美式发音: /ˌiː.kəˈnɑː.mɪk/ 或 /ˌɛk.əˈnɑː.mɪk/

Economics

- 英式发音: /ˌiː.kəˈnɒm.ɪks/

- 美式发音: /ˌiː.kəˈnɑː.mɪks/ 或 /ˌɛk.əˈnɑː.mɪks/

Economist

- 英式发音: /ɪˈkɒn.ə.mɪst/

- 美式发音: /ɪˈkɑː.nə.mɪst/

Economy

- 英式发音: /ɪˈkɒn.ə.mi/

- 美式发音: /ɪˈkɑː.nə.mi/

这些单词在英式英语和美式英语中的发音可能略有不同。希望这些音标对你有所帮助!

security: 证券

dividends: 美 [ˈdɪvəˌdendz] 股息;红利;被除数;(dividend的复数)

actuarial tables: 精算表格

archaeologist:美 [ˌɑːrkiˈɑːlədʒɪst] 考古学家

wheelbarrow:美 [ˈ(h)wilˌbɛroʊ] 手推车;独轮车

strap:美 [stræp] 带,皮带

trail:美 [treɪl] 拖;拉;拖沓行走;慢吞吞地走;

it would trail behind you 它会跟在你后面

aisle:美 [aɪl] 通道;走廊;过道 注意发音

subtitle:美 [ˈsʌbtaɪtl] 字幕, 注意发音

quirks:美 [kwɜrks] 怪癖;奇事;(quirk的复数)

enunciate:美 [əˈnənsiˌeɪt] 阐明;宣布;

But it was never enunciated as clearly as in 1811但它从未像1811年那样被清楚地阐明过

pursued:追赶;追捕;追击

investors in stocks can never be pursued for the mistakes of the company invested in 股票投资者永远不会因为所投资公司的错误而被追究责任

transgression:美 [trænzˈgreʃən] 违反;逸出;犯罪

This is going to lead to a wild transgression of our laws 这将导致严重违反我们的法律

mecca:美 [ˈmɛkə] 麦加;圣地;(mecca)朝拜的地方;

a mecca for business:商业圣地

nominal debt:名义债务

the government might print money, and debase the currency 政府可能会印钱,并使货币贬值

As Plato said, necessity is the mother of invention. 正如柏拉图所说,需要是发明之母。

rebellion:美 [rɪˈbeljən] 反叛;造反;叛乱

extol:美 [ɪkˈstoʊl] 颂扬;赞美

So here’s an invention that I’ve been extolling now for 25 years 这是一项我已经赞美了25年的发明

fluctuation: 波动

bizarre:美 [bɪˈzɑːr] 奇怪的

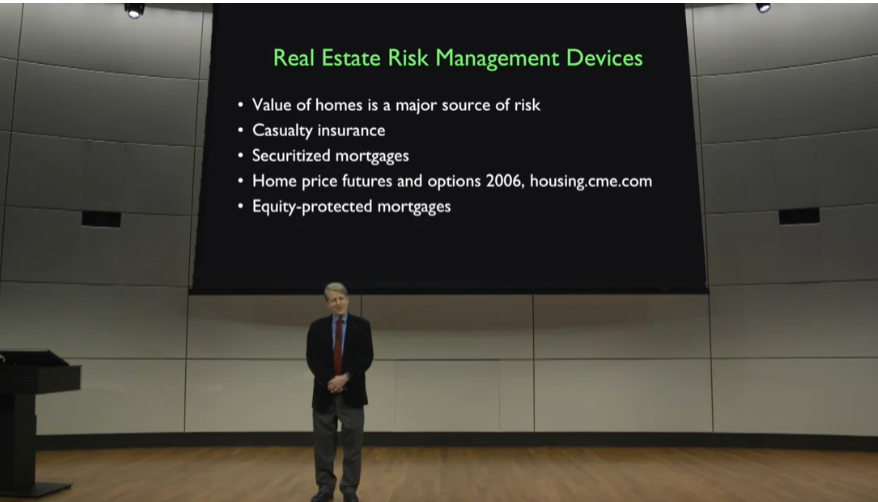

Finally, real estate risk management devices. Values of homes go up and down a lot and people are not protected against these fluctuations and this is bizarre to me. 最后,房地产风险管理工具。房屋价值大起大落,人们无法抵御这些波动,这对我来说很奇怪。

borne:美 [bɔːrn] 支持;支撑;

That is borne by you, the homeowner 这是由你这个房主承担的

lamp post 灯柱

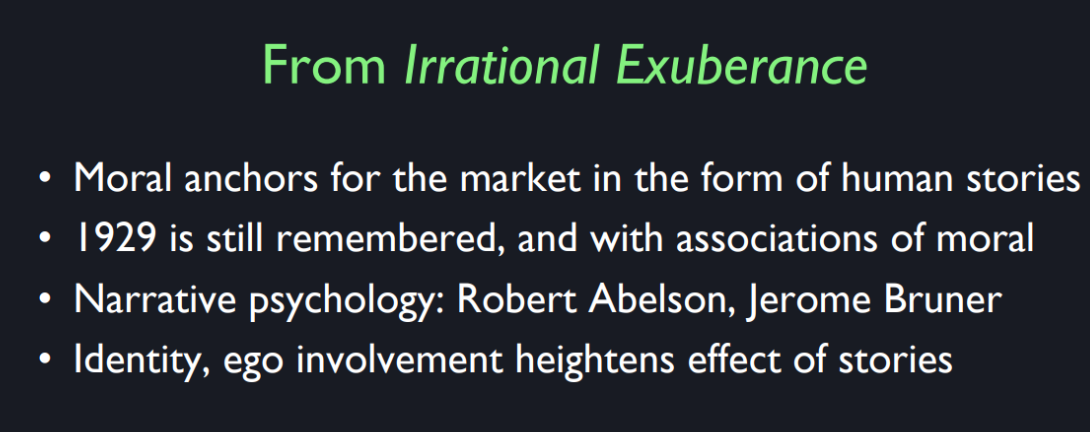

exuberance: 美 [ɪg’zjʊbərəns] 丰富;茂盛;充沛

irrational exuberance 非理性繁荣

beeper:呼叫器;传呼机;蜂鸣器

coiner:美 [ˈkɔɪnər] 铸造钱币者;新词的创造者

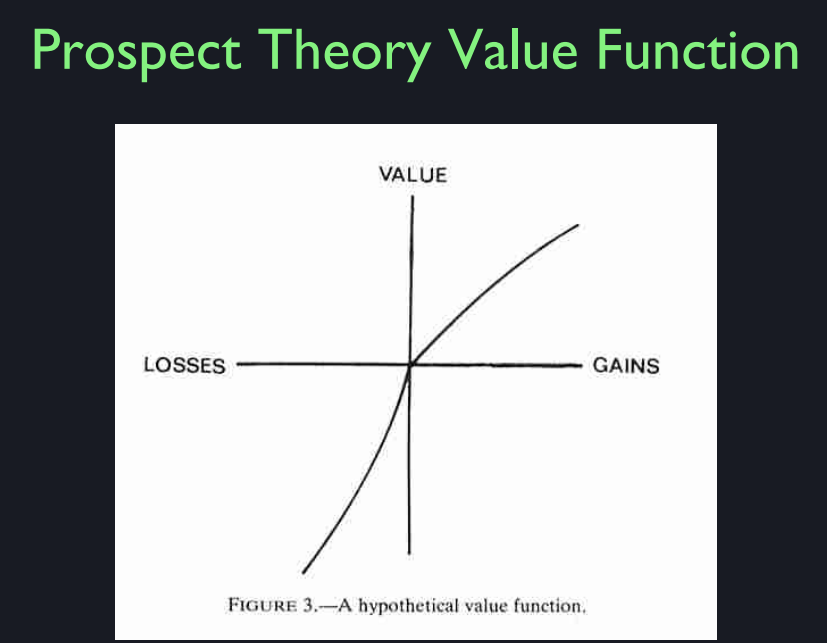

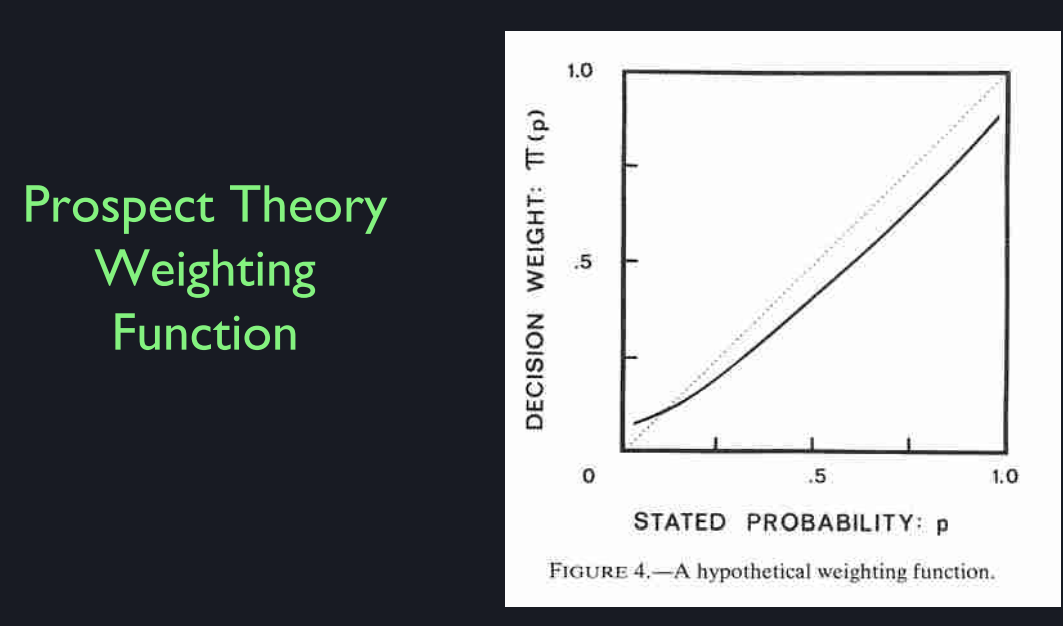

utility:效用

Expected Utility Theory: 预期效用理论

concave ( l o g x log x logx) or convex ( x 2 x^2 x2): 凹凸性

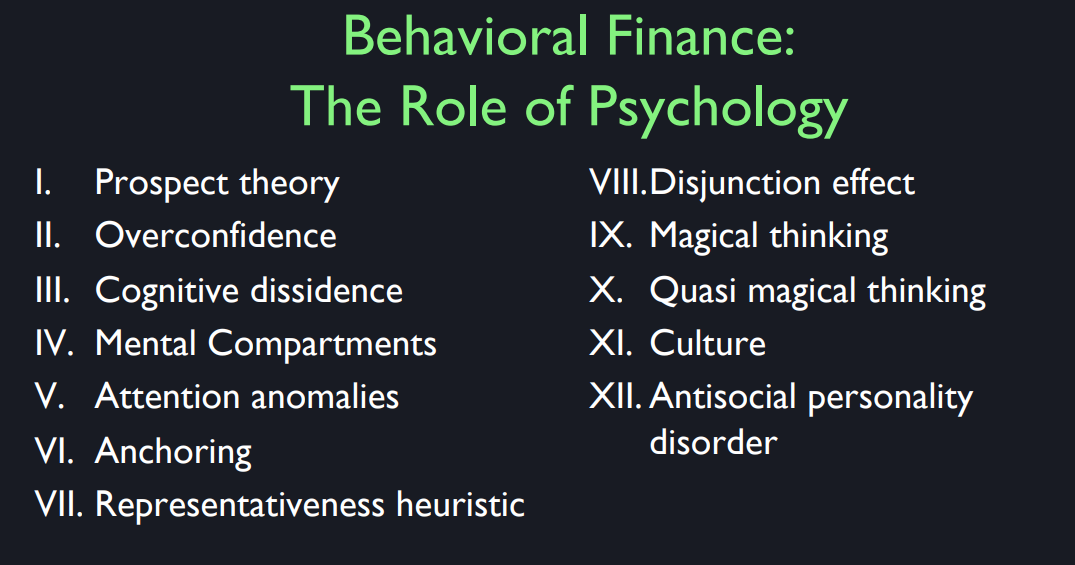

dissonance: 美 [ˈdɪsənəns] 不和谐;不一致;不协调

Cognitive dissonance: 认知不一致, 认知失调

compartment: 美 [kəmˈpɑːrtmənt] 分离部分;分隔的空间;

mental compartments 心理隔间

option: 期权

call option:看涨期权

put option:看跌期权

anomaly: 美 [əˈnɑːməli] 异常;反常现象;

attention anomalies:注意力异常

arbitrage:美 [ˈɑrbəˌtrɑʒ] 套利

no arbitrage assumption: 无套利假设

bank teller:银行出纳

sculptress:美 [ˈskəlptrəs] 女雕刻家;女雕塑家

And the choices involved bank teller or sculptress. 选择包括银行出纳员或女雕塑家。

disjunction: 美 [ˌdɪsˈdʒəŋ(k)ʃ(ə)n] 不对应;不一致;析取

disjunction effect: 分离效应

superstition: 美 [ˌsuːpərˈstɪʃn] 迷信;盲目的迷信想法

fallacy: 美 [ˈfæləsi] 谬论;谬见;谬误

contagion:美 [kənˈteɪdʒən] 传播;散布;蔓延

social contagion: 社交传播

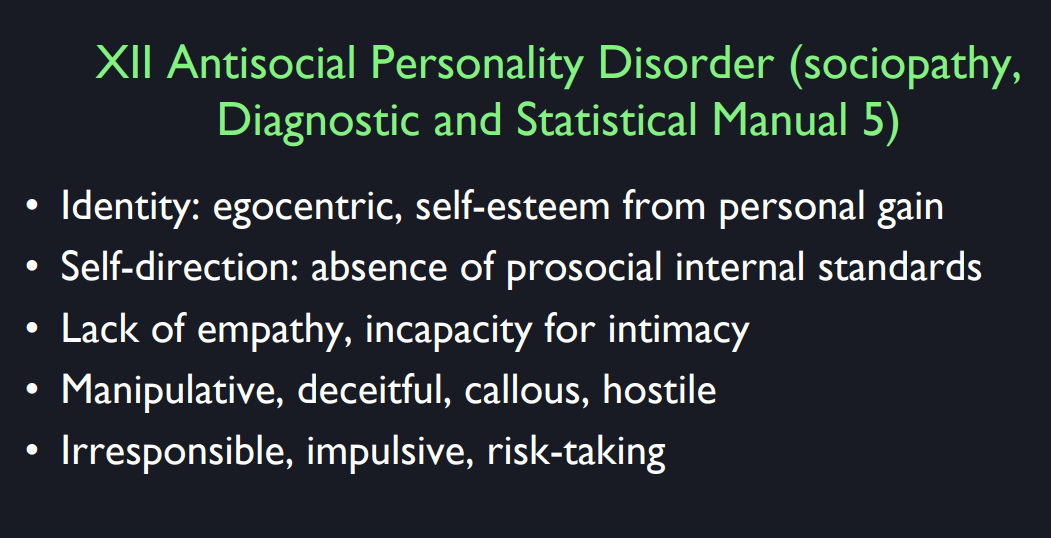

sociopathy:美 [sosiopæθi] 社会病态

Lesson #5

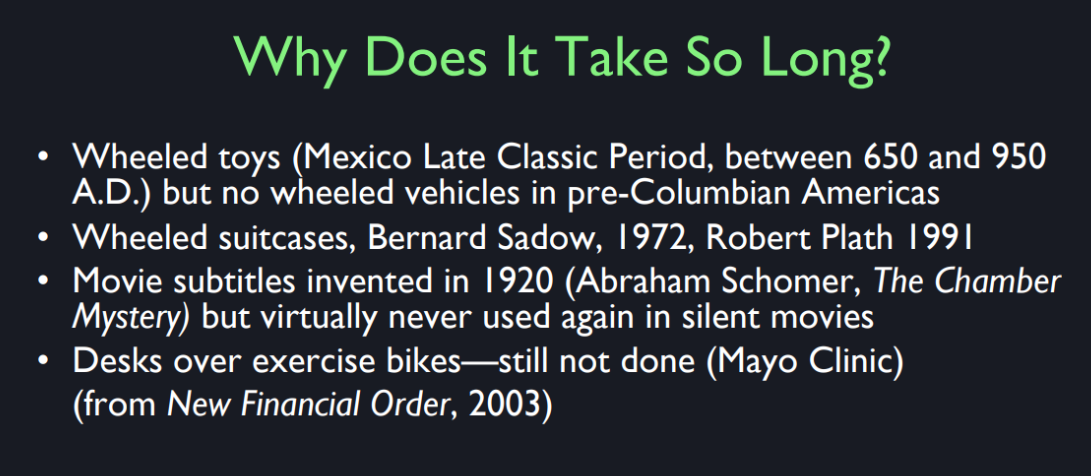

Invention Takes Time

Why does it take so

long for ideas to develop? l mentioned insurance,

it goes back to ancient Rome. Why is it that we didn’t have any real

insurance, l mean in the sense of an insurance company with actuarial

tables and the like, until the 1600s? And why did fire insurance

on homes become important? Most people didn’t own

fire insurance until after the reformations

in the Great Depression. So the funny thing about invention to me,

is that ideas that seem simple and natural, somehow don’t get established,

I’ll give you some examples. These are from my book,

The New Financial Order. Wheeled toys okay, well archaeologists in Mexico find that there were children’s

toys, that had wheels on them. Little toy cars, and you could roll

them along the floor all right, so they knew about wheels. But you know what, nowhere in

the Americas, did they ever find a wheeled wagon, or anything used. A wheelbarrow, nothing,

they only had toys, strange.

Now this brings up another

example of wheeled suitcases. So I wrote this book in 2003,

13 years ago, and you have a suitcase with wheels on it,

right? Does anyone not have

wheels on their suitcase? Well it seems like this is so obvious,

suitcases should have wheels. But you know they didn’t until 1972? That’s not long ago, and in fact,

I was doing research for my book, and I had an undergraduate research assistant. And I was intrigued by

these wheeled suitcases. So I asked my student go find

the inventor, is he still alive? So he tracked him down,

it was Bernard Sadow in 1972. And called him up on the phone,

again inventors don’t tend to be famous. You didn’t know his name, right? It’s changed your life. [LAUGH] You don’t know what is

like carrying a heavy suitcase when there are no wheels on it. So my student asked him what was it

like inventing the wheeled suitcase? And he said, I had a lot of resistance, I showed my wheeled suitcases,

I went to department stores. Remember department stores? They used to have those

instead of online shopping. And I told them, this is a great idea,

and they said, no it isn’t, nobody’s going to buy that. It looks ridiculous, wheels on suitcases.

They said look, if you want help with

your luggage, every train station, every hotel has porters who will be ready

to help you, you don’t need these things. That’s what they told him, but

he did get some of them to sell. The problem with his wheeled suitcase,

however now he didn’t get it right either. He had a suitcase,

a big suitcase like this, and there were four little tiny wheels on

the bottom, and there was a strap, right? So you would pull on the strap

like a leather strap, and it would trail behind you. You might still have one

in your parents’ attic. They flop over, that’s the problem, you

start pulling and it falls over sideways. But you can do it, you can figure

out eventually how to pull it. It wasn’t until Robert Plath in 1991,

invented something he called the Rollaboard,

which you now have, right? And actually, it improved again. But in 1991, he had a suitcase with

just two wheels on the bottom, and a rigid handle,

not this leather strap. And the handle collapsed into

the suitcase, and you could pull it out, and then would tilt, and

it would be very stable. That was 1991, and

that just completely took over. He called it a Rollerboard,

because he was an airline pilot, and he made it narrow enough so

you could roll the suitcase down the aisle of the airplane, and

it wouldn’t bump into anyone. It was under control. You know what the latest thing is? It’s like a Rollaboard,

I’m going on too long about this. The latest thing is now they

have four wheels again. And you can either do it

like a Rollaboard, or you can stand it up, and people like that. Every one of these

inventions took ten years. You’d think Bernard Sadow would’ve

figured the whole thing out in 91, but that’s not the way it works.

Movie subtitles were invented in 1920, but never really used in silent movies,

I think this is amazing. They had this whole silent movie era,

they’d already invented subtitles, and they didn’t put them on movies. They had these intertitles,

you remember silent movies? They would stop the whole movie and

they’d show you this intertitle. But it’s so much better, and

I’m really used to it now. You can watch a movie with, it doesn’t

matter what language it’s in anymore. So obvious.

And desks over exercise bikes,

I have this in my basement. I put a desk over my exercise bike,

and I’m preparing my lecture. Mayo Clinic is selling them now,

but it’s a slow thing. Eventually you ought to get one,

so that you can exercise and do scholarly work at the same time.

I think that we’re moving ahead. Another way of putting it is,

financial theory and practice are good areas for

young people to go into, because I think it has been transforming and

will continue to be transforming. And I think that the nature of our

financial markets in 10, 20, 30, 50 years, which matters for young people today,

will be amazingly different and better. And you have to join the financial

community to make that happen, you don’t have to, I’m just saying. >> [LAUGH]

Do you have in your mind, an ideal of what future looks like? >> See there are people who proposed

like Karl Marx for example. >> Right. >> Robert Owen who’s the guy

who coined the term socialism. They had ideals which they sold on

the public as simple and obvious. >> Right. >> But I think it’s not quite so

simple and obvious. The human species is

the product of evolution, that gave us a number of different mental

quirks that served us well as cavemen. [LAUGH] But now they don’t really

fit into the modern world, we’re just seeing new opportunities. So we might be excessively fearful or

unwilling to change. We might be too focused on

our own personal lives. And we have to invent something different,

and it won’t be a perfect world, just like it’s never been a perfect world,

but it’s exciting and it’s getting better.

Salon - Innovation

What do you think has been

important about the innovation of people’s ability to insure

against risk in the marketplace? Whether it’s through just something

as simple as an insurance contract or by other means? >> Well, the history of risk management

goes back thousands of years. I would say that the history

of risk management is, the technology that we have has been

very slow to develop over the centuries. And that encourages me to think that

it has a lot more to develop yet, a lot more to develop yet. I think that there’s

an inherent conservationism and mistrust of new financial arrangements. In the sense that, I’m not coming to this party unless

the in-people coming to it also. And so things are very slow to develop. I don’t know if I’m

answering your question. It is a belief of mine that financial innovation is a pillar

of our civilization. That it’s not just

shifting papers around and getting people to sign documents that

trick them into signing away something. It’s a sequence of inventions

that incentivize people, provide capital for enterprises. Create organizations that last

through time that separate themselves from the objectives of the individuals

who comprise the corporation. And get people focused on some

common good that will be produced.

Do you think it’s safe

to say that historically, financial innovation has

occurred on the upside? Looking to capture new markets and

new ways of earning returns, versus on the, kind of the downside

risk management side of the ledger. >> Well, when we say risk management,

it seems to imply a focus on the downside. But it’s on the upside as well,

because people accept the downside risk because there’s something on the plus

side that is enticing and is exciting. So this is an interesting point, people seem to like gambles that involve a small amount of money

lost with high probability. And a large money gained

with low probability. So if that’s what people like,

we have to try to turn the natural risks which might be balanced equally into loss

and gain into something more appealing. So that’s one thing that

limited liability did.

People like lottery tickets. I paid $2 today, and

I have the chance of winning $10 million. For some reason, the chance is minuscule. It’s virtually zero, but

somehow people like that. So that’s a discovery of our human nature. Why they like that is a puzzle but

we just know that people like that. It’s because people savor

the small probability. I have this lottery ticket

I bought this morning. I could be worth $10 million at the end

of the day when they announce the number. That just makes your day bright. And then, when you don’t win, you still

feel well, it was just $2, so what. So what limited liability

does is it creates that for corporate, that same sense for

investing in stock. You bought 100 shares,

so maybe that’s $3,000. That’s a little bit more

than a lottery ticket. But hey, I could be a multimillionaire

if I bought the right company. It’s like a lottery ticket. So people flock to these things. And they’re actually,

they’re disappointed almost always. But they’re not disappointed

because we end up with a more vital business sector

where things are created. So we have to try to reframe things. That’s what part of

financial innovation is. Reframe risk so that they’re appealing. And we want to also, for good social

purpose to be risks that need to be taken. So that they benefit the economy.

Here’s a summary of the professor’s key points:

Slow Development of Risk Management Technology:

- The history of risk management spans thousands of years but has developed very slowly.

- There is inherent conservatism and mistrust in new financial arrangements, causing slow adoption and innovation.

Financial Innovation as a Pillar of Civilization:

- Financial innovation is crucial for civilization, not just about paperwork or contracts.

- It provides capital for enterprises, creates lasting organizations, and focuses on common good beyond individual objectives.

Focus on Upside and Downside Risk Management:

- Risk management often implies focusing on downside risks, but it includes upside opportunities.

- People accept downside risks because of enticing upside gains, which is a key part of financial innovation.

Human Nature and Risk Preferences:

- People prefer gambles with small losses and large potential gains (e.g., lottery tickets).

- This preference can be harnessed through financial instruments like limited liability, which makes investing in stocks similar to buying lottery tickets.

Limited Liability and Investment Appeal:

- Limited liability appeals to investors by providing a chance of high returns while limiting losses, akin to the appeal of lottery tickets.

- This encourages investment and creates a more dynamic business sector.

Reframing Risk for Economic Benefit:

- Financial innovation involves reframing risks to make them appealing and beneficial for the economy.

- By doing so, necessary risks are taken, leading to overall economic growth and development.

The professor emphasizes the importance of financial innovation in managing both risks and opportunities, its slow historical development, and the psychological factors influencing investment behavior.

以下是教授要点的总结:

风险管理技术的发展缓慢:

- 风险管理的历史可以追溯到数千年前,但其技术发展非常缓慢。

- 对新金融安排的保守态度和不信任导致了这种缓慢的采纳和创新。

金融创新是文明的支柱:

- 金融创新对文明至关重要,不仅仅是处理文件或签订合同。

- 它为企业提供资本,创建持久的组织,并关注超越个人目标的共同利益。

侧重于上下风险管理:

- 风险管理通常意味着关注下行风险,但它也包括上行机会。

- 人们接受下行风险是因为上行收益具有吸引力,这是金融创新的关键部分。

人性与风险偏好:

- 人们倾向于接受小额损失和潜在大额收益的赌博(例如,买彩票)。

- 这种偏好可以通过有限责任等金融工具来利用,使股票投资类似于购买彩票。

有限责任与投资吸引力:

- 有限责任通过提供高回报的机会,同时限制损失,使投资者感到投资类似于购买彩票。

- 这鼓励了投资,创造了更具活力的商业部门。

为经济利益重新定义风险:

- 金融创新涉及重新定义风险,使其更具吸引力并有利于经济。

- 通过这样做,必要的风险得以承担,从而促进整体经济增长和发展。

教授强调了金融创新在管理风险和机遇中的重要性,它的历史性缓慢发展,以及影响投资行为的心理因素。

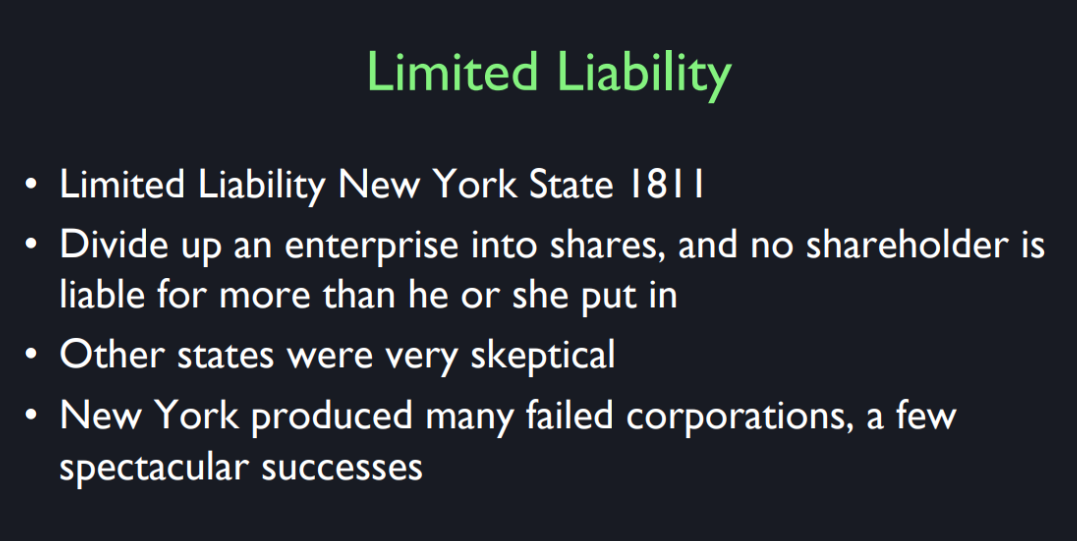

Limited Liability

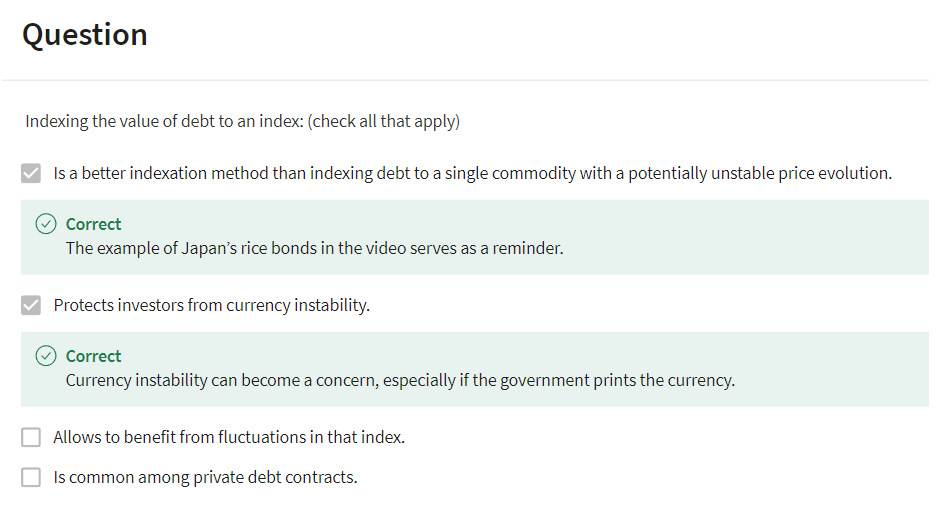

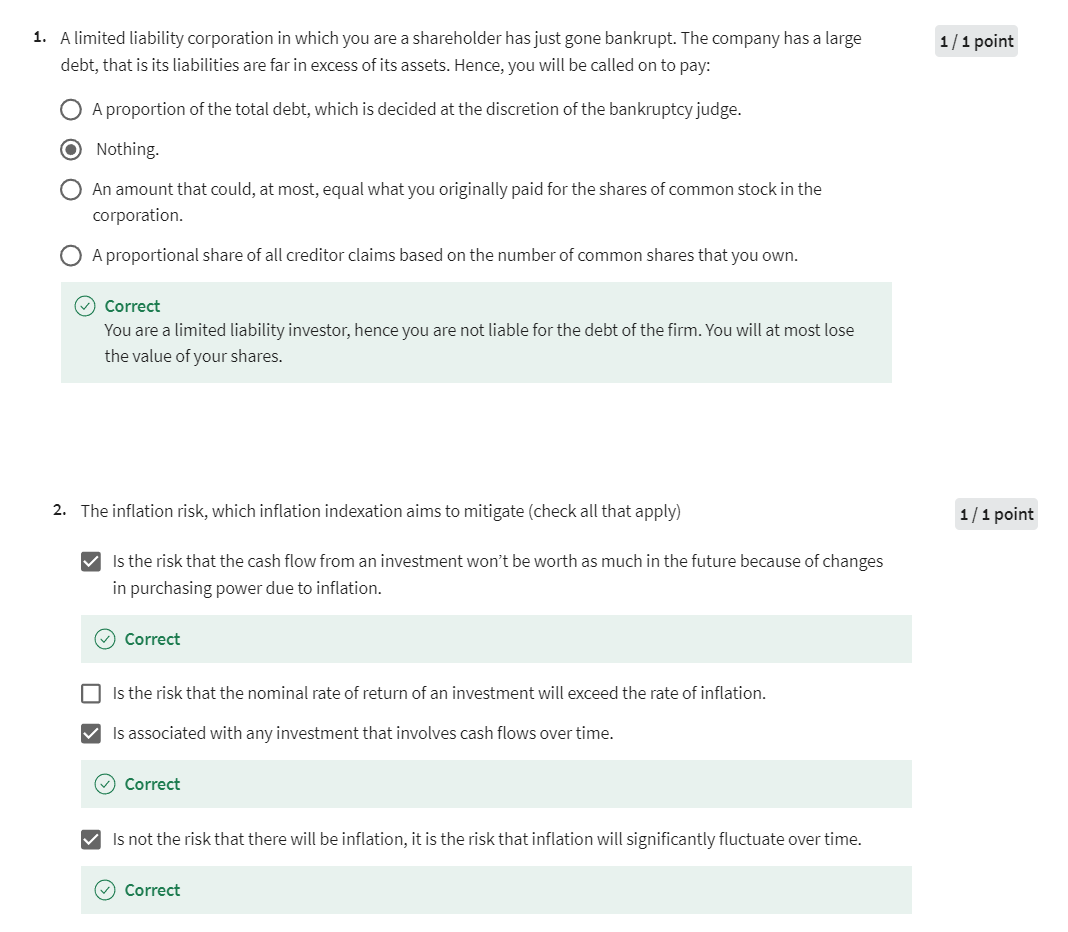

So I wanted to give some examples, both from the past and from the things that I’ve talked about now. So, the first example I like is limited liability. I’m going to credit New York State with inventing the full dimension of this idea in 1811. However, it precedes the idea of limited liability, it precedes 1811 and I don’t know what country can be given credit for discovering it. But here is the idea.

Well, actually it goes back in a way to Bottomley which I talked about. The idea is that investors, in order to be encouraged to invest in businesses, should have protection against liability for what the managers of the business do. They should have limited liability. So the example we gave before, is if you’re in ancient Rome and you are considering investing in a trade, a trip where they’re going to send out a ship to trade goods, if the ship sinks, you are not liable. You don’t have to pay the loan back. That’s an example. But it was never enunciated as clearly as in 1811.

So New York State passed a new law then, that said investors in stocks can never be pursued for the mistakes of the company invested in. So what we’re going to do is allow it. Well, already they had shares. You could buy shares in businesses but you only are liable for what you put in initially, and no more worries. So - but before this law, there was doubt about that. Apparently the idea of going after shareholders for the sins of a company was rare, but people had to worry about so this is what could happen. Before 1811 in New York, you could buy shares in some company and then the company commits a crime and then they come after you to pay up for the crimes of the managers. And you say, “I didn’t know. You know, I just bought some shares. I didn’t know who these guys were.” And they would say, “Well. tough luck. Pay up or go to debtors’ prison.” That’s what they would potentially do. And they had debtors’ prison. There was a different idea there, but the idea is if you invested in this company, you are responsible and we’re not going to forgive you.

So when New York State passed the law, there was a lot of controversy and a lot of people in other states said, "This is crazy. People are not responsible for what they invest in and what happens. This is going to lead to a wild transgression of our laws and our - Massachusetts passed a law, similarly around the same time, reaffirming that shareholders are responsible for what they invest in, you are a party to the crime. So what happened? Well, almost all of the business went to New York and New York became a mecca for business. And eventually, gradually, state by state, they all did it. They all passed limited liability laws. There were a few spectacular failures, you know corrupt businesses. But so many good businesses started this way. So I think this was an invention, and it was an experiment in human nature. The problem is that people, if you are responsible for everything you get involved in, then you won’t do it. You won’t supply capital to some business.

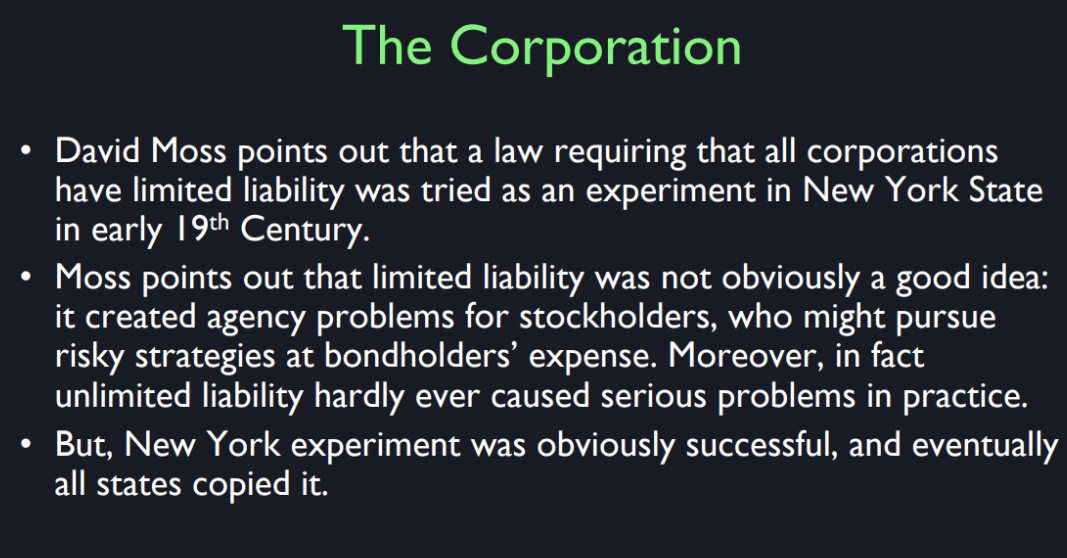

David Moss was a graduate. I mentioned him before, a graduate student here at Yale who wrote his dissertation and then a book called, “When all else fails, the role of government in risk management.” He describes this controversy in 1811. But the real genius of limited liability is that it makes it possible for you to make an investment in some enterprise and then it’s just fun. There are no more - you can lose what you put in, but you know exactly what you put in. So what Moss said in his book is that it’s really behavioral. You know, this is human factors engineering. Nobody knew when they tried limited liability what would happen. It might encourage corruption. It might not affect the supply of capital.

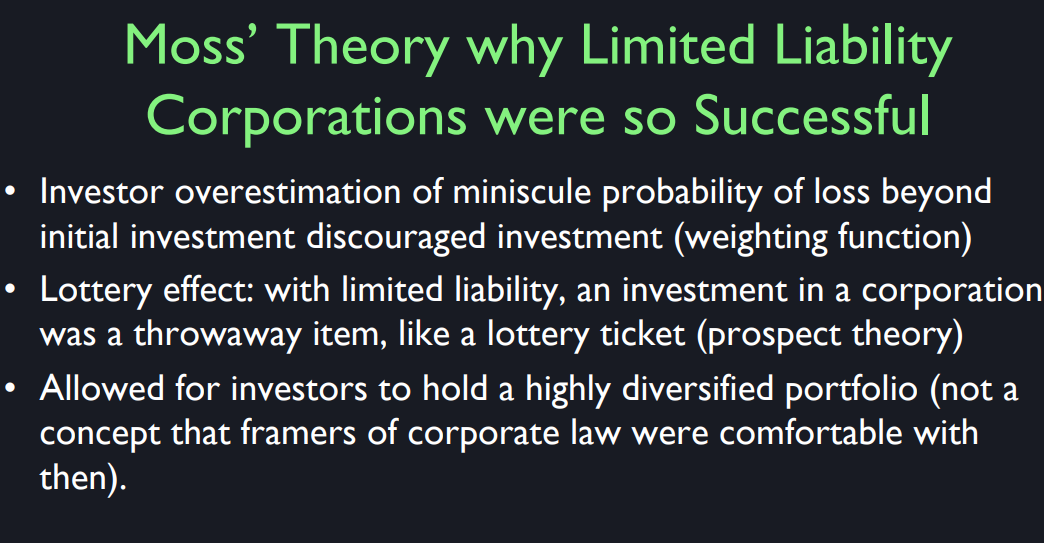

But we discovered that investor psychology favors limited liability. That’s because investors tend to- if they’re not limited liability, they overestimate the minuscule probability of loss. Just as when they buy lottery tickets, they over estimate the minimal probability of winning. So he thought that what the limited liability did, is created a sort of lottery effect. People are basically you know, you’re driven toward fun things and you don’t like things that make you worry. So let’s make it buying a share in some startup company is like buying a lottery ticket. And, now you probably won’t get rich almost certainly won’t get rich, but hey it’s fun. And so, just like lotteries, I don’t know why people- when I go to the train station, I have to stand in line at the little store there behind people buying lottery ticket. I can’t imagine why me or anyone would buy those, because your chance of winning is so low. But people do buy and they just it makes their day, I guess they have fun. You buy a lottery ticket in the morning and then where do you turn on television? I don’t know. There’s some television clip that shows you them drawing the ball, and you’re all excited and you’re having fun and you lose. You think they keep losing, that they would stop that they don’t. There’s something- you wouldn’t know this but that’s human nature. The other thing about limited liability, is that it created the whole idea of holding a diversified portfolio. If you don’t have limited liability, absolutely not. You should not hold a diversified portfolio. Especially if you have some wealth, they’ll go after you. One of those companies is going to go down and they’ll go after you. So, don’t hold that diversified portfolio. Once they discovered that- once they did limited liability, then you could start enjoying your investment and diversify over many things. And we know that there is risk management power in the diversification.

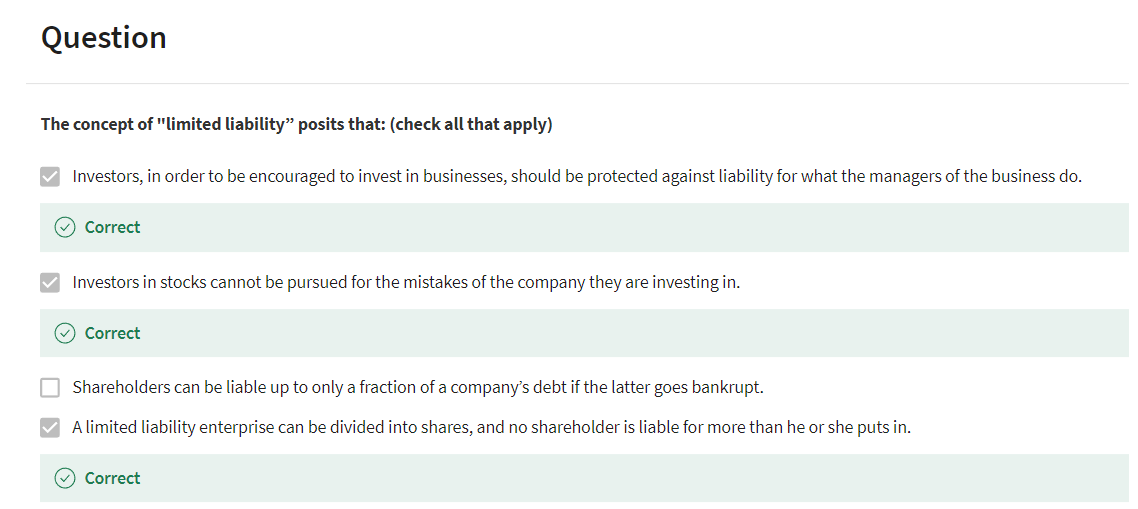

Investors in stocks cannot be pursued for the mistakes of the company they are investing in. 股票投资者不能因为所投资公司的错误而被追究责任。

Investors, in order to be encouraged to invest in businesses, should be protected against liability for what the managers of the business do. 为了鼓励投资者投资于企业,投资者应该受到保护,不为企业管理者的行为承担责任。

A limited liability enterprise can be divided into shares, and no shareholder is liable for more than he or she puts in. 有限责任企业可以分成股份,任何股东都不必为超过其投入的部分承担责任。

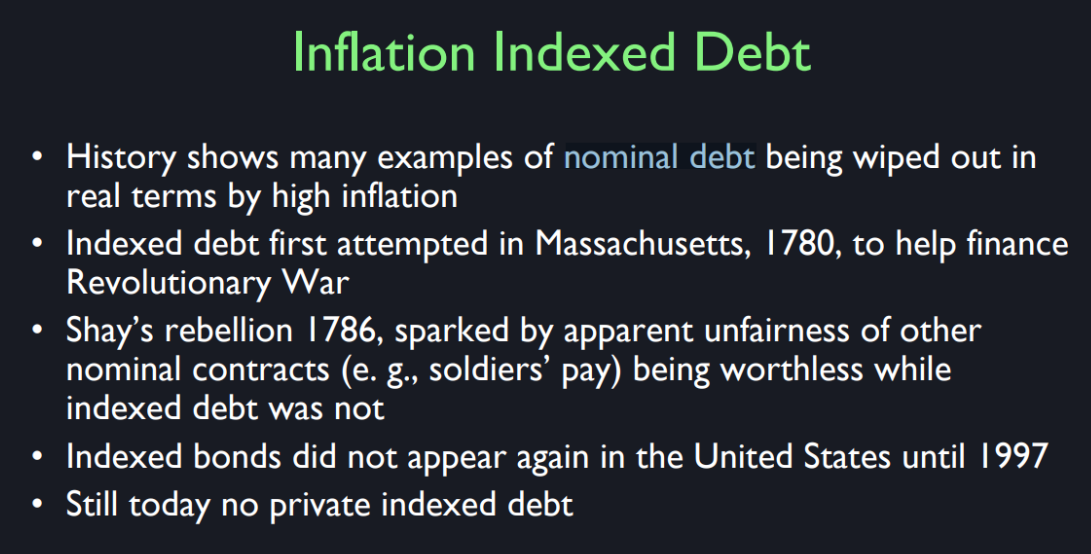

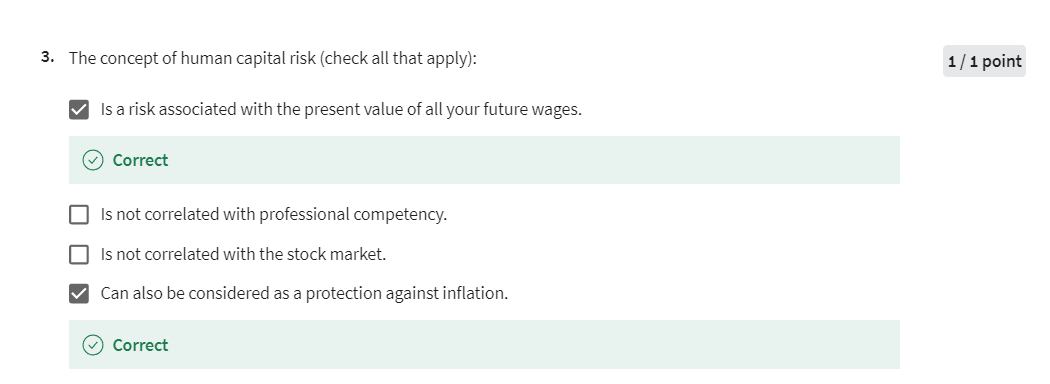

Inflation Indexed Debt

So I give you another example of

practical financial innovation. Towards here about inflation indexed debt. So we’ve always traditionally

borrowed money in debt contracts and promised to pay them back in the currency. But there are so many examples

where the currency is unstable, especially if the government prints it. They make big mistakes. So, the idea is,

why don’t we have a price index and have a debt contract that

pays back index to inflation? Then it’s fixed in real terms. What could be more obvious? But the history of it is very slow to get going. I’ve tried to find who is

the first person to define that in terms of a consumer price index. There were earlier examples. For example, in Japan, they had rice

bonds, and maybe other places too. So a rice bond was a debt instrument

that was payable in rice, yes, the grain, instead of a currency. And you’re safer with that than in

currency if the government might print money, and debase the currency. But the idea that I’m referring

to is something broader. The problem with rice bonds

is the price of rice isn’t stable relative to other prices. So you really want an index of prices. You want to tie the contract to an index. So, as far as I’ve been able to tell,

I wrote a paper about this.

The first indexed debt was invented

here in the United States in 1780, and it occurred because of inflation. The US Government was giving debt to the soldiers during the revolutionary war, denominated in currency that was

issued then by state governments. And they debase the currency because

of the war, it was rapid inflation. And the soldiers were really

unhappy because what they got was already worthless before they got it. And in order to keep the soldiers happy,

this was a necessity. As Plato said,

necessity is the mother of invention. He was quoting someone else, I believe,

but that’s where it appears. So they decided to define

a consumer price index. They didn’t call it that,

they just defined it. And the bond had to pay out

in inflation-indexed terms. And what a wonderful idea, its simple. You should promise them in real terms

not money terms, and then inflation. But there was a lot of other

people were paid in nominal debts. And there was an actual rebellion called

Shays’ rebellion about the unfairness of this debt. So, somehow the US government

didn’t issue them again.

Well, the indexed bonds in 1780

were issued by Massachusetts, but no state issued indexed

bonds again until 1997. I can’t believe that it took so long. I was there advocating, this is one

thing I advocated before it happened. Not that that necessarily made

a difference, but I just wonder about. It seemed impossible. I called treasury like in 1996 and

I said, I want to talk to someone here, why don’t you do inflation-indexed debt? And I got a guy on the phone and

he said, we’d thought of that. We have a joke here at treasury. And that is that if we ever do

issue inflation-indexed debt in the United States, we should send

the prospectuses to the members of the American Economic Association. because they’re the only ones

who would be interested. I said, how can that be? I mean, people are getting the real value

of their debt wiped out by inflation, don’t they care? I mean, and it still puzzles me

that it isn’t more important. People just don’t get it, they make

the same mistake again and again. They think, well, inflation is only 2%. But they don’t know that history shows

that governments messed up all the time. Now of course, this is America,

we don’t mess up here, I guess, you could say it patriotic feeling. You don’t want to raise the possibility

that we would mess up and have a lot of inflation. But maybe even if it isn’t a lot,

maybe how about 4% a year inflation, and you lose half your money

in 20 something years. That’s within the realm of possibility,

people don’t even think about it. But we do have inflation-indexed

debt in the United States, and it has spread around the world. Now, the US was not the beginning

of inflation-indexed debt in 1997, it was in 1780, I believe.

通胀指数债务(Inflation-indexed debt)指的是本金和/或利息支付会根据通胀率进行调整的一种债券或贷款。这种调整帮助保护投资的价值免受通胀侵蚀。

具体来说,对于通胀指数债券,本金额会定期根据特定的通胀指数(如消费者价格指数,CPI)进行调整。因此,利息支付也会随着通胀的变化而增加或减少,因为利息是根据调整后的本金计算的。

这意味着,如果通胀上升,债券的本金和利息支付都会增加,从而保护投资资金的购买力。反之,如果出现通缩,本金和利息支付可能会减少。

通胀指数债务的例子包括:

- 美国的通胀保值债券(TIPS)。

- 英国的指数联动国债(Index-linked gilts)。

- 加拿大的实值回报债券(RRBs)。

这些金融工具对于担心通胀会侵蚀其固定收益投资实际价值的投资者特别有吸引力。

Inflation-indexed debt refers to a type of bond or loan where the principal and/or interest payments are adjusted according to inflation rates. This adjustment helps protect the value of the investment against the eroding effects of inflation.

For instance, in the case of inflation-indexed bonds, the principal amount is adjusted periodically based on a specified inflation index, such as the Consumer Price Index (CPI). As a result, the interest payments, which are calculated as a percentage of the principal, also increase or decrease in line with inflation.

In practice, this means that if inflation rises, both the principal value and the interest payments of the bond will increase, preserving the purchasing power of the invested funds. Conversely, if there is deflation, the principal and interest payments may decrease.

Examples of inflation-indexed debt include:

- Treasury Inflation-Protected Securities (TIPS) in the United States.

- Index-linked gilts in the United Kingdom.

- Real Return Bonds (RRBs) in Canada.

These financial instruments are particularly attractive to investors who are concerned about inflation eroding the real value of their fixed-income investments.

**通胀指数债务(Inflation-indexed debt)**有着相对悠久的历史和广泛的应用。以下是其发展历史的简要概述以及当前的受欢迎程度:

历史背景

早期发展:

- 英国:世界上最早的通胀指数债券可以追溯到英国。英国政府在1981年首次发行了通胀指数债券(Index-linked Gilts),以保护投资者免受通胀影响。

其他国家的引入:

- 美国:美国在1997年引入了通胀保值债券(TIPS,Treasury Inflation-Protected Securities),这些债券使投资者能够获得与通胀挂钩的收益。

- 加拿大:加拿大在1991年发行了其首个通胀指数债券,称为实值回报债券(RRBs,Real Return Bonds)。

- 其他国家:许多其他国家随后也开始发行通胀指数债券,包括澳大利亚、瑞典和意大利等。

当前的受欢迎程度

在现代金融市场中,通胀指数债券继续受到投资者的青睐,特别是在以下情境下:

- 通胀预期上升:当市场预期未来通胀上升时,通胀指数债券变得特别有吸引力,因为它们能够保护投资者的购买力。

- 低利率环境:在低利率环境中,固定收益投资的实际回报率可能较低。通胀指数债券提供了一种保护手段,能够抵御潜在的通胀风险。

- 养老基金和长期投资:由于通胀指数债券提供了抵御通胀的保障,许多养老基金和长期投资者将其纳入投资组合,以确保长期购买力的稳定。

当前市场趋势

虽然通胀指数债券在某些时期会更受欢迎,但它们始终是投资组合中重要的组成部分,尤其对于那些希望在不确定的通胀环境中保护其投资的人而言。

- 市场波动:通胀预期和经济不确定性(如疫情、地缘政治风险等)常常会影响这些债券的受欢迎程度。

- 机构投资者的偏好:大型机构投资者,如养老基金、保险公司和主权财富基金,通常会将通胀指数债券视为对冲通胀风险的重要工具。

总结

通胀指数债务具有重要的历史背景和显著的市场价值。尽管其受欢迎程度可能随着经济环境和通胀预期的变化而波动,但它始终是金融市场中重要的一类工具,尤其对于那些寻求长期稳定回报的投资者而言。

History of Inflation-Indexed Debt

Early Development:

- United Kingdom: The earliest example of inflation-indexed bonds can be traced back to the UK. The British government first issued inflation-indexed bonds, known as Index-linked Gilts, in 1981 to protect investors from inflation.

Adoption by Other Countries:

- United States: The U.S. introduced Treasury Inflation-Protected Securities (TIPS) in 1997, allowing investors to receive returns linked to inflation.

- Canada: Canada issued its first inflation-indexed bond, called Real Return Bonds (RRBs), in 1991.

- Other Countries: Many other nations followed suit, including Australia, Sweden, and Italy.

Current Popularity

Inflation-indexed bonds remain popular among investors, particularly in certain contexts:

- Rising Inflation Expectations: When the market expects future inflation to rise, inflation-indexed bonds become particularly attractive because they protect investors’ purchasing power.

- Low-Interest Rate Environment: In a low-interest-rate environment, the real returns on fixed-income investments may be low. Inflation-indexed bonds offer a way to hedge against potential inflation risks.

- Pension Funds and Long-Term Investors: Due to their ability to protect against inflation, many pension funds and long-term investors include inflation-indexed bonds in their portfolios to ensure stable long-term purchasing power.

Current Market Trends

While the popularity of inflation-indexed bonds can fluctuate, they remain an important component of investment portfolios, especially for those seeking protection in uncertain inflationary environments.

- Market Volatility: Inflation expectations and economic uncertainties (such as pandemics, geopolitical risks, etc.) often influence the demand for these bonds.

- Institutional Investors’ Preference: Large institutional investors, like pension funds, insurance companies, and sovereign wealth funds, typically view inflation-indexed bonds as crucial tools for hedging against inflation risks.

Summary

Inflation-indexed debt has a significant historical background and considerable market value. Although their popularity may vary with changes in the economic environment and inflation expectations, they consistently serve as an essential tool in financial markets, particularly for those seeking long-term stable returns.

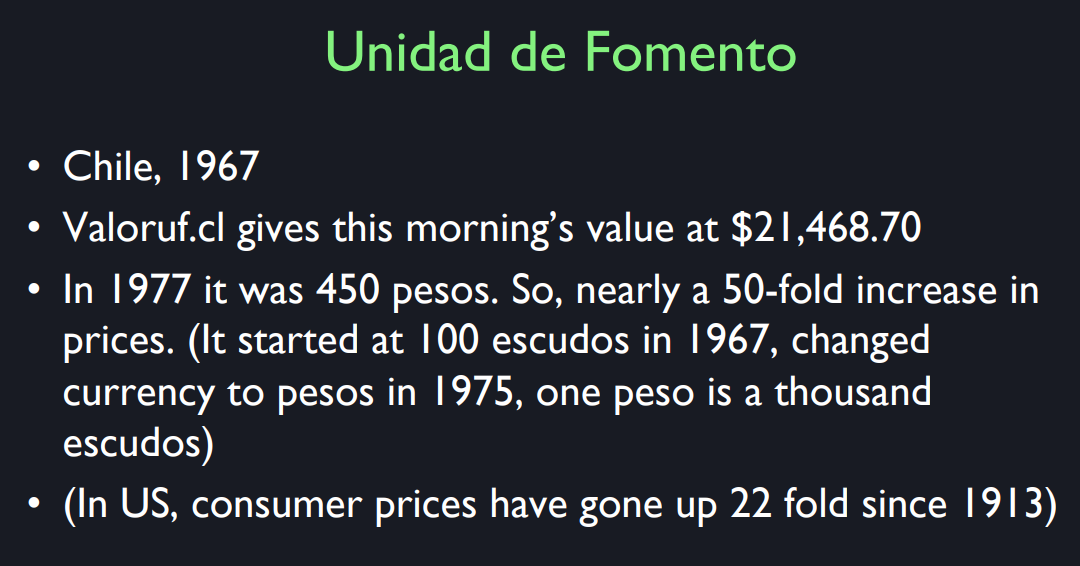

Unidad de Fomento

So here’s an invention that I’ve

been extolling now for 25 years. So far, I will note, well,

I shouldn’t say no success. I’ve gotten attention for it. But I think it won’t

happen in my lifetime, but we’ll do the Unidad de Fomento eventually. It’s coming. So let me tell you the invention. In 1967,

Chile was going through a hyperinflation. I mean, prices were just going up. I don’t know what it was,

1,000% a year or something like that. And people were distressed about it. When you got your paycheck,

you know what you did? You got your paycheck. Of course, you cash it immediately and you run to the store and

you spend the whole thing. Because by the end of the month,

[LAUGH] it won’t be worth anything. [LAUGH] So this is crazy. And so now the idea that Chile invented then was to create a new unit of account. In Spanish, unidad de fomento,

which means unit of development. I don’t know why they called it that,

but I can think of a better name. But that’s what they called it in 1967.

Now money has several functions. It’s a store value and a unit of

account and a means of transactions. You can separate out those functions. You can have a separate unit

of account that is not money. So they invented something called the UF,

a Unidad de Fomento, and they allowed its value to be

tied to the Consumer Price Index. Back then, they would publish in Chilean

newspapers every day the exchange rate between the, Escudo, which was the currency they had then,

and the UF. So I looked it up today. Now it’s a website,

used to be in the newspaper. Well, maybe it’s still in the newspapers. But there’s a website, valoruf.cl. I looked it up this morning and 1 uf is 25,655.55 pesos. Now you might wonder,

why did they pick such a big number? They didn’t, they picked some small, maybe

it was one to one, I don’t know exactly, in 1967. But they’ve had so

much inflation in their peso, that it’s up to 25,000 pesos per 1 UF. And that is worth,

at the current exchange rate, between peso and dollar, $35.92. So there’s been a huge increase, even though Chile has gotten its

inflation more under control, the price level has

still increased 50-fold, over 50-fold, since 1977. But the US is not the haven

of price stability either. Would you believe it, prices in the US

have gone up 24-fold since 1913? That’s not exactly a zero

inflation environment. And if you’re saving for your retirement,

for example, your grandmother buys you a savings bond that matures in 2050,

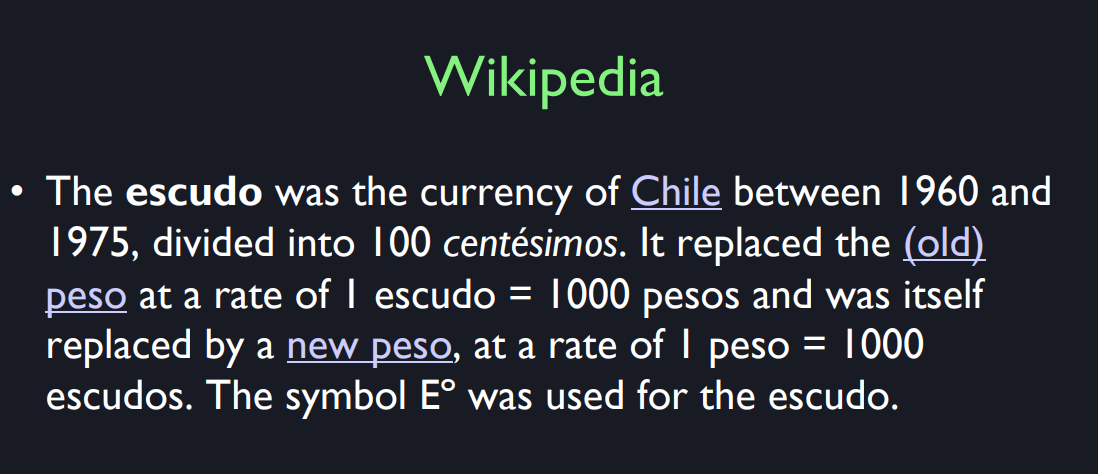

you should be worried, right? What is that going to be worth? So Chile had the escudo currency,

and between 1960 and 1975, they had so much inflation that they had to replace it with 1

escudo to 1,000 pesos. But then the peso then eroded away,

and they had to define a new peso, which was 1,000 old pesos. So we have something like a 50 million

fold increase in prices in Chile.

So why would anybody still

quote prices in pesos? I don’t know. There’s something about human psychology. But at least let’s give credit. The Chileans are the most advanced

country in the world in terms of dealing with inflation. When I was in Chile, I was giving

a talk at the Central Bank, and I said, whose idea was this? This is amazing. The whole world should be following to it. And then, you know what? Nobody knew whose idea it was, nobody. They think it’s a national embarrassment

because it reveals how much inflation they’ve had. I said, no, you are the world’s leader,

and the world ought to copy you. Eventually, they will.

Unidad de Fomento(UF) 是智利的一种货币单位,主要用于调整和衡量经济活动中的货币价值,以应对通货膨胀带来的影响。UF的价值每天都会根据前一天的通货膨胀率进行调整。其主要特点和用途如下:

通货膨胀调整:

- UF的价值每天会根据智利的消费价格指数(CPI)进行调整,因此它能反映出货币的实际购买力。

- 这种调整机制使UF在通货膨胀期间保持相对稳定,保护货币价值不受通货膨胀的侵蚀。

使用场景:

- 房地产交易:很多房地产买卖合同和租赁协议都是以UF计价的。这可以防止因通货膨胀导致的货币贬值对合同金额的影响。

- 金融合同:银行贷款、抵押贷款和其他长期金融合同也常用UF计价。

- 公共服务费用:一些公共服务和公用事业费用也以UF计价,以保持费用的实际价值。

- 储蓄和投资:某些储蓄账户、保险合同和年金也会以UF计价,以确保其价值不会因通货膨胀而减少。

计算与发布:

- 智利中央银行负责计算并发布UF的每日价值。UF的价值通常在各大媒体和银行网站上公布,方便公众查阅。

历史背景:

- UF于1967年首次引入,目的是为了在高通货膨胀环境下提供一种稳定的价值衡量单位。自引入以来,UF已经成为智利经济中不可或缺的一部分。

总之,Unidad de Fomento 是一种旨在对抗通货膨胀影响的货币单位,通过每日调整其价值,使其在各种金融和经济交易中提供一种相对稳定的价值参考。这种机制在高通胀经济体中尤为重要,有助于确保合同和金融资产的实际价值不因通货膨胀而显著减少。

Unidad de Fomento (UF) is a unit of account used in Chile, primarily designed to adjust and measure the value of economic activities to counteract the effects of inflation. Here are its main features and uses:

Inflation Adjustment:

- The value of the UF is adjusted daily based on the previous day’s inflation rate, as measured by the Consumer Price Index (CPI) in Chile.

- This adjustment mechanism allows the UF to maintain a relatively stable purchasing power during periods of inflation.

Use Cases:

- Real Estate Transactions: Many real estate purchase contracts and rental agreements are denominated in UF. This prevents the devaluation of contract amounts due to inflation.

- Financial Contracts: Bank loans, mortgages, and other long-term financial agreements are often priced in UF.

- Public Service Fees: Some public services and utility charges are also priced in UF to maintain the real value of fees.

- Savings and Investments: Certain savings accounts, insurance contracts, and annuities are denominated in UF to ensure their value is protected from inflation.

Calculation and Publication:

- The Central Bank of Chile is responsible for calculating and publishing the daily value of the UF. The value is typically available in major media outlets and on bank websites for public reference.

Historical Background:

- The UF was introduced in 1967 to provide a stable unit of value in an environment of high inflation. Since its introduction, the UF has become an integral part of the Chilean economy.

In summary, the Unidad de Fomento is a monetary unit designed to combat the effects of inflation by adjusting its value daily. This mechanism is crucial in high-inflation economies, ensuring that contracts and financial assets retain their real value over time.

**通货膨胀(Inflation)和货币贬值(Currency Depreciation)**之间有密切的关系,但它们是不同的经济现象。下面解释它们之间的关系,并通过具体例子说明。

通货膨胀

通货膨胀是指物价普遍上涨的现象,导致货币购买力下降。换句话说,同样数量的货币在未来能够购买的商品和服务会比现在少。

货币贬值

货币贬值是指一种货币相对于其他货币的价值下降。通常是由于市场供求关系、经济政策、政治稳定性等因素导致的。

二者的关系

通货膨胀可以导致货币贬值,尤其是在通货膨胀率较高的情况下,因为高通货膨胀率往往会削弱外国投资者对该国货币的信心,导致该国货币对其他货币的汇率下降。

具体例子

例子:委内瑞拉的经济危机

通货膨胀:

- 背景: 委内瑞拉经历了多年经济动荡,政府过度发行货币以应对经济困境。

- 结果: 物价飞速上涨。例如,2018年委内瑞拉的通货膨胀率达到惊人的1,000,000%。

- 影响: 人们发现日常必需品如食品和药品的价格每天都在上涨。同样数量的玻利瓦尔(委内瑞拉货币)今天能够购买的物品,在明天可能只能购买一半甚至更少。

货币贬值:

- 背景: 由于国内严重的通货膨胀和经济不稳定,外国投资者失去了对委内瑞拉经济和玻利瓦尔的信心。

- 结果: 玻利瓦尔对美元等主要外币的汇率迅速下跌。例如,2018年初1美元约等于10玻利瓦尔,但到年底,1美元已经等于约248,000玻利瓦尔。

- 影响: 国际贸易成本大幅增加,进口商品价格飞涨,进一步加剧了国内的通货膨胀。

总结

通货膨胀和货币贬值相互影响。高通货膨胀会削弱货币的购买力,从而导致国际市场上该国货币的贬值。反过来,货币贬值也会使进口商品价格上涨,进一步推动国内通货膨胀。通过委内瑞拉的例子,我们可以看到这种恶性循环的实际影响。

Exchange rates of Renminbi

汇率是指一种货币相对于另一种货币的价格,它在国际贸易和金融活动中起着至关重要的作用。以人民币(CNY)和美元(USD)为例,可以更清楚地说明汇率的作用。

- 国际贸易

汇率直接影响到进出口商品的价格。

- 人民币贬值:如果人民币对美元贬值,例如从1美元兑换6.5元人民币变为1美元兑换7元人民币,中国的出口商品对美国买家来说变得更便宜,这可能会刺激美国对中国商品的需求。同时,美国的出口商品对中国买家来说变得更贵,这可能会减少中国对美国商品的需求。

- 人民币升值:如果人民币对美元升值,例如从1美元兑换6.5元人民币变为1美元兑换6元人民币,中国的出口商品对美国买家来说变得更贵,可能会减少美国对中国商品的需求。同时,美国的出口商品对中国买家来说变得更便宜,这可能会增加中国对美国商品的需求。

- 投资流动

汇率影响外国投资者在某国投资的成本和收益。

- 人民币贬值:如果人民币对美元贬值,外国投资者可能会发现他们的投资收益在兑换成美元时减少,从而降低他们在中国投资的意愿。

- 人民币升值:如果人民币对美元升值,外国投资者可能会发现他们的投资收益在兑换成美元时增加,从而增加他们在中国投资的意愿。

- 通货膨胀和物价水平

汇率变动对国内的物价水平和通货膨胀有直接影响。

- 人民币贬值:进口商品和原材料的成本上升,导致国内生产成本增加,进而推动物价上涨,可能引发通货膨胀。

- 人民币升值:进口商品和原材料的成本下降,可以抑制国内物价上涨的压力,甚至可能导致通货紧缩。

- 货币政策

中央银行可以通过干预外汇市场来影响汇率,从而实现宏观经济目标。

- 外汇干预:中国人民银行可以通过买卖外汇储备来影响人民币汇率。例如,卖出美元、买入人民币可以支撑人民币汇率,防止其过度贬值;反之,买入美元、卖出人民币可以抑制人民币升值。

- 利率调整:调整利率也可以影响汇率。提高利率可以吸引外国资本流入,推高人民币汇率;降低利率可以促使资本外流,压低人民币汇率。

- 旅游和教育

汇率影响旅游和留学的成本。

- 人民币贬值:中国居民出国旅游或留学的成本增加,因为他们需要更多的人民币兑换成外币。

- 人民币升值:出国旅游或留学的成本降低,中国居民更容易支付这些费用。

实际例子

- 中美贸易战:在中美贸易战期间,人民币对美元曾有贬值趋势。中国通过适度让人民币贬值,使得中国出口商品对美国更加有价格竞争力,以部分抵消美国关税的影响。

- 留学费用:假设某中国学生需要支付每年3万美元的学费。当汇率是1美元=6.5元人民币时,这需要支付195,000元人民币。如果人民币升值到1美元=6元人民币,那么只需要支付180,000元人民币,学费变得更便宜。

总结

汇率在国际贸易、投资、物价水平、货币政策以及个人消费等多个方面都起着重要作用。汇率波动会对经济产生广泛的影响,因此各国政府和企业都密切关注汇率变化并采取相应措施应对。

Exchange rates represent the value of one currency relative to another and play a crucial role in international trade, investment, and financial activities. Using the exchange rate between the Chinese Yuan (CNY) and the US Dollar (USD) as an example, we can better understand the importance and implications of exchange rates.

- International Trade

Exchange rates directly affect the prices of imported and exported goods.

- Renminbi Depreciation: If the Chinese Yuan depreciates against the US Dollar, for example, from 1 USD = 6.5 CNY to 1 USD = 7 CNY, Chinese exports become cheaper for American buyers. This could increase demand for Chinese goods in the US. Conversely, US exports become more expensive for Chinese buyers, potentially reducing demand for US goods in China.

- Renminbi Appreciation: If the Chinese Yuan appreciates against the US Dollar, for example, from 1 USD = 6.5 CNY to 1 USD = 6 CNY, Chinese exports become more expensive for American buyers, potentially decreasing demand for Chinese goods in the US. Conversely, US exports become cheaper for Chinese buyers, potentially increasing demand for US goods in China.

- Investment Flows

Exchange rates impact the cost and returns of foreign investments.

- Renminbi Depreciation: If the Yuan depreciates, foreign investors might see their investment returns decrease when converted back to their home currency, which could reduce their willingness to invest in China.

- Renminbi Appreciation: If the Yuan appreciates, foreign investors might see their investment returns increase when converted back to their home currency, which could increase their willingness to invest in China.

- Inflation and Price Levels

Exchange rate fluctuations affect domestic price levels and inflation.

- Renminbi Depreciation: The cost of imported goods and raw materials rises, increasing domestic production costs and potentially leading to higher prices and inflation.

- Renminbi Appreciation: The cost of imported goods and raw materials falls, reducing domestic price pressures and potentially leading to lower inflation or even deflation.

- Monetary Policy

Central banks can intervene in the foreign exchange market to influence exchange rates and achieve macroeconomic goals.

- Foreign Exchange Intervention: The People’s Bank of China can buy or sell foreign exchange reserves to influence the Yuan’s exchange rate. For example, selling US Dollars and buying Yuan can support the Yuan’s value, preventing excessive depreciation. Conversely, buying US Dollars and selling Yuan can curb the Yuan’s appreciation.

- Interest Rate Adjustments: Adjusting interest rates can also impact exchange rates. Raising interest rates can attract foreign capital inflows, increasing the Yuan’s value. Lowering interest rates can encourage capital outflows, decreasing the Yuan’s value.

- Tourism and Education

Exchange rates affect the cost of travel and education abroad.

- Renminbi Depreciation: Traveling or studying abroad becomes more expensive for Chinese residents, as they need more Yuan to exchange for foreign currency.

- Renminbi Appreciation: Traveling or studying abroad becomes cheaper for Chinese residents, as they need fewer Yuan to exchange for foreign currency.

Real-world Example

- US-China Trade War: During the US-China trade war, the Chinese Yuan experienced depreciation against the US Dollar. By allowing the Yuan to depreciate moderately, China made its exports more price-competitive in the US market, partially offsetting the impact of US tariffs.

- Study Abroad Costs: Suppose a Chinese student needs to pay $30,000 annually for tuition. When the exchange rate is 1 USD = 6.5 CNY, the cost in Yuan is 195,000 CNY. If the Yuan appreciates to 1 USD = 6 CNY, the cost drops to 180,000 CNY, making tuition more affordable.

Conclusion

Exchange rates are vital in various aspects of the economy, including international trade, investment, price stability, monetary policy, and personal consumption. Exchange rate fluctuations can have widespread economic impacts, prompting governments and businesses to closely monitor and respond to these changes.

Real Estate: Risk Management Devices

Finally, real estate risk management devices. Values of homes go up and down a lot and people are not protected against these fluctuations and this is bizarre to me. We have home insurance, casualty insurance that protects you against accidents in your home or you get protection against fires so why not protect them against the big risk, which is the change in value of your home. Are people who do things like short the financial markets good people or bad people? Shorting, is it evil to short a market? Well, if you’re shorting a market for homes in your own city, you’re just trying to protect yourself against the collapse. It’s not so evil. If you’re doing it to make billions of dollars it’s a little bit ambiguous, your moral stance. But anyway it’s legal, you can short markets and I thought it would be a good thing if people could short the housing market. It would help stop bubbles and it would help people protect themselves against this. There could also be a source of risk management for equity protected mortgages. You should have a mortgage that tells you when you buy a house, if your home price falls below the amount you owe, we’ll correct your debt downward. Isn’t that sensible? But that’s not what we did, not what we are doing. If you buy a house for $500,000, you borrow $450,000, the price of the house falls to 400,000, you are now $50,000 underwater. You go into your mortgage lender and you say, "I’m underwater. What do we do? " And the mortgage lender will typically say, “Tough luck, we’ll sue you. We’l go after you if you don’t pay?” Why do we leave it like that? Well, it’s because progress is slow.

When you talk a lot about financial innovations is there anything of recent that is really credit for you or that you think it’s, kind of, the next frontier of finance? There are many innovations. I don’t know where to begin. Well, but let me put it this way that most of our risks are still not managed well, for example, your home price risk. That is borne by you, the homeowner. I actually work with the Chicago Mercantile Exchange and we do have a futures market for single, and an options market, for single family homes so that you can buy a put option on your house to protect you against the big fall. That is up and running. I want to see it grow and get more more active but it is, it does exist. Another risk which is even bigger is the risk of your human capital that you are investing in now as a student. And now, you are an MBA student so you have chosen a very fungible form of human capital management. That has to be a very versatile skill that right, at least that sounds like it to me, that won’t be replaced by a computer. Now, it might be partly replaced by computers, in fact, it already has partly been replaced, I think. But, I think, that’s, but the question is, what if you pick a human capital that is more focused, like nuclear engineering. Now you could, how can you protect yourself against that risk to your human capital? Well, I have an idea how you could do it. You could short the stock of a nuclear power company, assume that it’s going to correlate negatively with your risk, so you can sort of do it. But I think there are other things that might be more appropriate for most people. I think that’s kind of requires some sophistication to pick a company and short it to protect yourself, your own human capital. President Obama in his State of the Union address for 2016 proposed wage insurance that when people lose their job and switch to a permanent job with a lower wage, there should be some pay out that would, insurance pay off for the loss of livelihood. I’ve advocated things like that, too, in my writings. I call it livelihood insurance. But I can keep coming up with there’s so many innovations and we don’t know which ones, but what we do know is that risk is not well-managed worldwide. And we also know that enterprises are not functioning well everywhere, that there are many places in the world where free enterprise and entrepreneurship seems limited, so there’s a lot of things to be innovated.

Lesson #5 Quiz

Lesson #6

Forecasting

So today I want to talk about

the Efficient Markets Hypothesis. The history of the hypothesis, reasons

to think that markets are efficient, and reasons to doubt it. Let me start with the dinner

experiment on Friday.

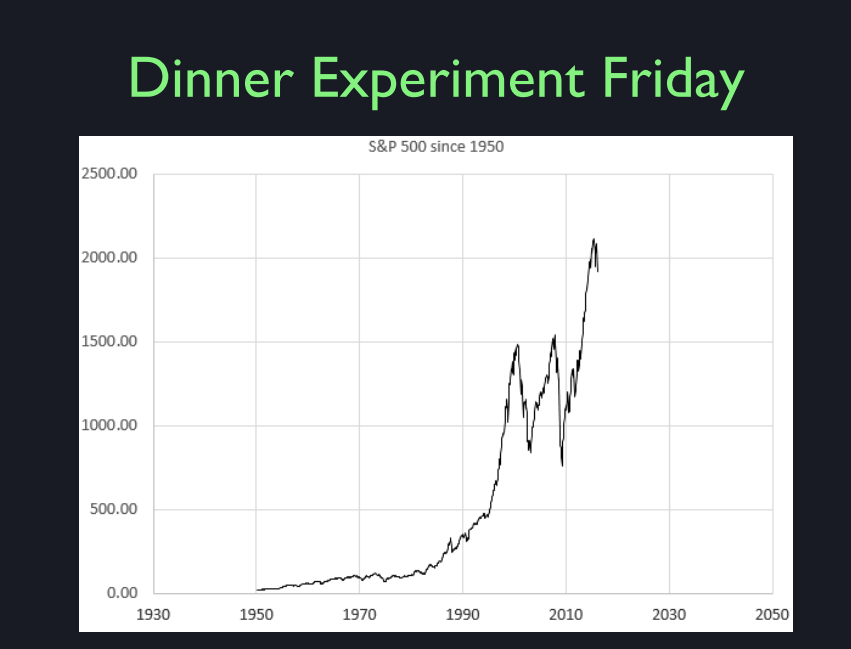

So we had a nice dinner at

Berkeley College, and as an experiment, those of you who were there

will know my experiment. I passed out slips of

paper with this chart. So the chart shows

the Standard & Poor’s 500 from 1950 until a couple days ago where it was. There it is, that is the stock market. And then I left room on the right,

up to the year 2050. And I asked each of you independently, and I asked you not to look at

each other when you did this, to pencil in a forecast for

the stock market from 2016 to 2050. So I’ll just give you a couple

examples that you filled in, this person is forecasting,

what does that look like? Another 20% drop in the market. Then a correction, then a drop, and then another boom, and

then another crash, and then another boom. So, I picked this one out as

just typical of what was seen. I should have shown you more, I only have

one other here, this is another one. So you are very pessimistic bunch.

What would Efficient Market Theory

say should be the forecast? There are one or two of you actually

did that, or maybe it was three, so more or less. If markets are completely unforecastable,

what should it be? Well, one interpretation

of efficient market, your forecast should have been zoom,

straight across, it’s not going to leave. I mean, the central tendency is, tomorrow’s price is

the same as today’s price. Because I can’t forecast changes up or

down, who knows? That would be efficient markets. But there is another version

of efficient markets and some of you actually did this,

but not many of you. Your forecast would be

not straight across but perfectly growing exponentially

along an exponential growth path. That would be the efficient

markets hypothesis taking account of the fact

that there’s a growth.

It’s not a random walk, but

it’s a random walk with growth. But almost none of you did that. Maybe my instructions

weren’t clear enough. But what you’re doing is

showing plausible paths for the stock market rather the expected path. That’s how people seem to interpret

when I say, please forecast it. You are trying to show what’s plausible. So you’re making,

if you look at the recent history, this person made it look like

the recent history, right? But this is not unless you can tell me,

I don’t know who did this forecast. But unless you can tell me, why did you have a turning point here in,

what year is that? 2020, why did you have this turning point, why did you have this turning

point where you put it? They have no reason, this looked plausible

to them so they called that a forecast. I know you might have done better if

you had more time to think about it. But I think this gets back to, it’s related to a concept in behavioral

economics that and talked about, those are two psychologists,

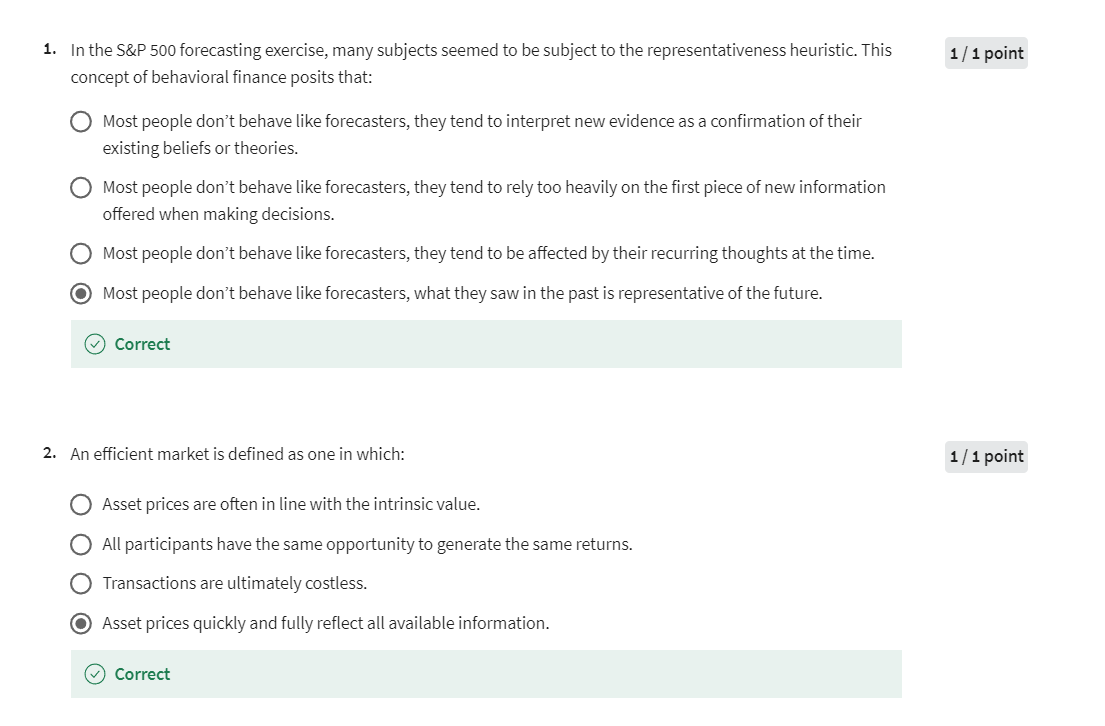

called the representativeness heuristic. People don’t behave like forecasters. They think that something

they saw in the past is representative of what

will happen in the future. Now I’m not defining their theory exactly,

but I think this is how most people take

it when they have to give a forecast.

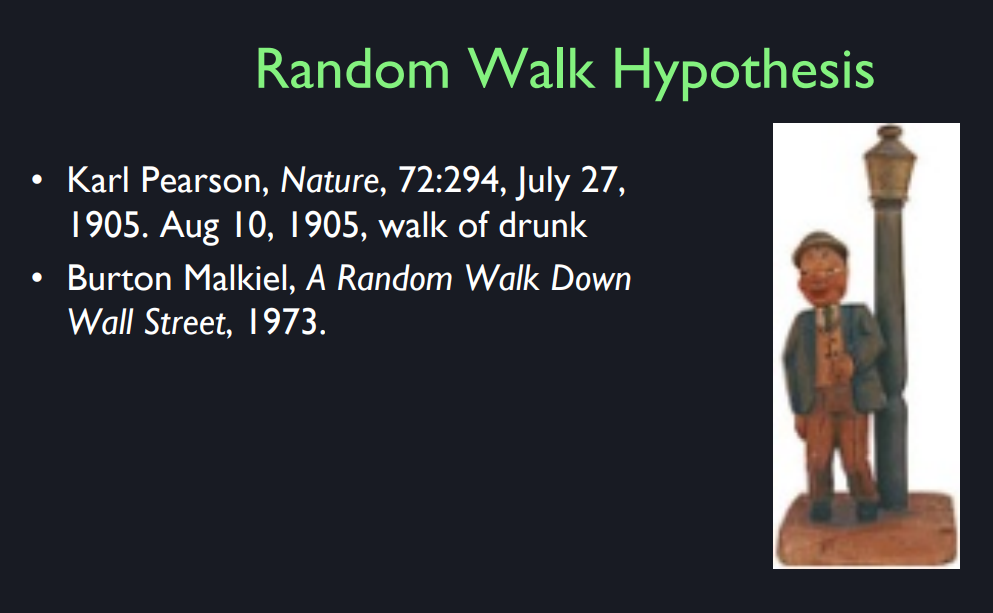

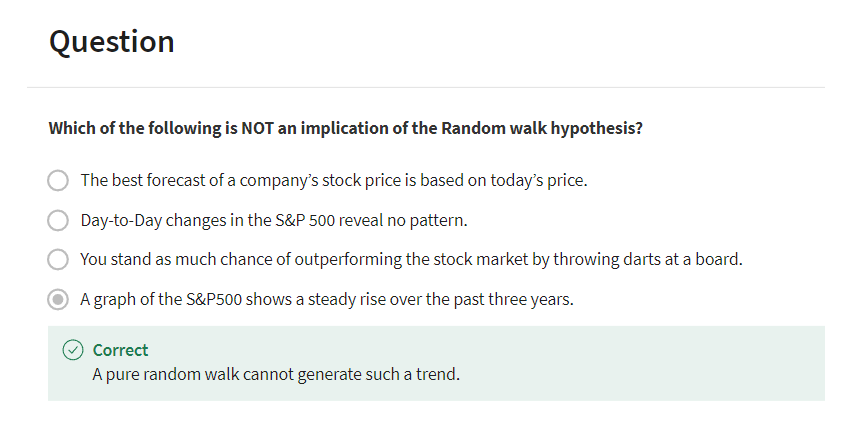

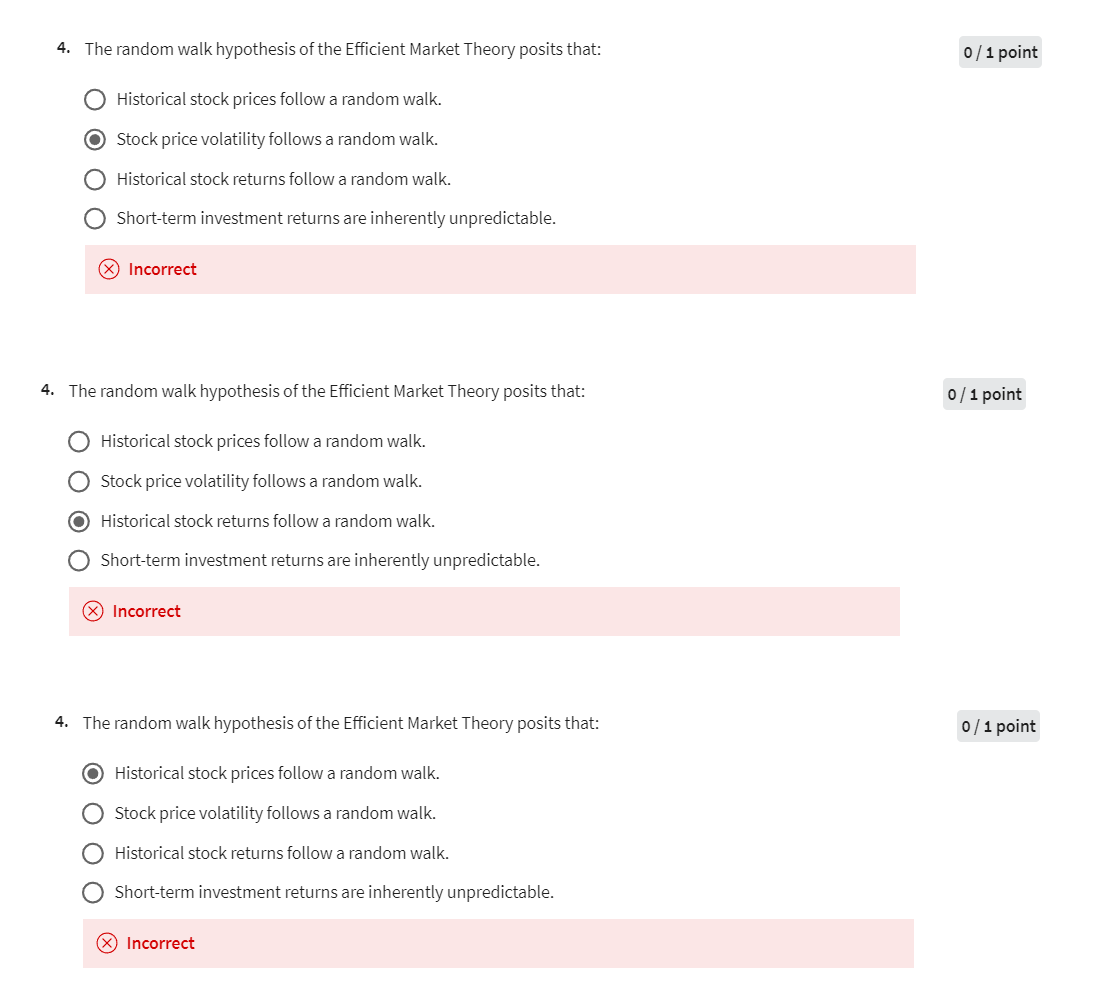

The random walk theory is a theory,

first, the term was coined by statistician Karl Pearson in

the scientific journal Nature in 1905. And he said,

a random walk is a process that changes in such a way that each

change is independent of previous changes and

totally unforecastable. So it has become popular

lore to think of a random walk as the walk of a drunk

at a lamp post, okay? And this toy, right here, is a mock-up that someone once made and

sold. If you want that,

I found it on the web, you can buy it. It’s amazing [LAUGH]

what you can buy today. But there’s your drunk. Now if the drunk is so totally drunk

that every step is completely random, so your job, according to Pearson, is to forecast the position

of the drunk in 10 minutes, in 20 minutes, in 30 minutes, okay? So what is your forecast? What do you think? What would be Karl Pearson’s forecast? Well, the forecast is he’s going to

be right at the lamp post. And the reason you’d make that as your

forecast is you have no idea whether it’s to the right, or to the left, or

whatever the direction is random. So he’s probably not going to

be at the lamp post but since you can’t predict which way, you

might as well predict at the lamp post. That’s why I was saying on the previous

slide that, I’ll go back here. Your forecast should have been zoom

straight across if stocks are few or random walk. But that’s not what you did.

In 1973, Burton Malkiel who was

a professor at Princeton and, I guess, still is, he came to Yale for some years

as Dean of the Yale School of Management. But he wrote a best selling book in 1973

called A Random Walk Down Wall Street, arguing that, it wasn’t original in

the book, this was a popularization. But it’s a best seller and

it sold millions of copies. The idea was coming out then that stock

market prices are really random walks, it’s all an illusion that you

think you can forecast it. So, you shouldn’t try to forecast it. You should just hold

a diversified portfolio. And that became conventional wisdom,

starting around that time.

Burton Malkiel, his book was very well

timed and a very appropriate title. The funny thing about Malkiel’s book,

though, is that he didn’t really believe the efficient market hypothesis

that he made the title of his book. Because if you look in at

the last chapter of the book, he had investing advice and he told

you to do various things that, well, I thought inconsistent with

random walk hypothesis. I finally met him at a cocktail party. And I asked him, I said, some of your investment advice

doesn’t quite fit with random walk. And then he said, well, I know. I can’t quote him exactly, so

I can’t get these other kinds of thinking completely out of my mind,

something like that. So, it’s like psychologically, we’re not

attuned to understand the random walk.

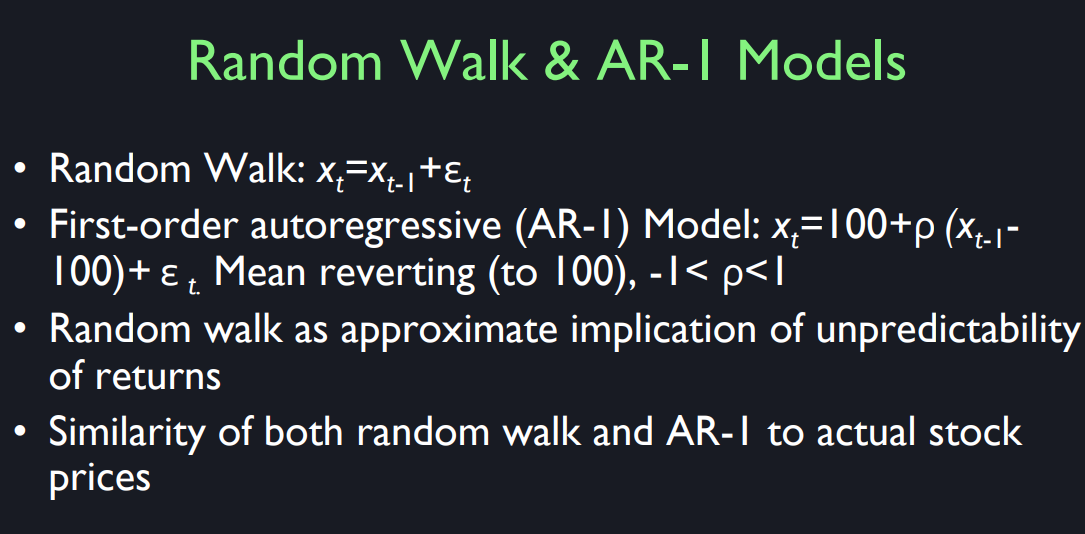

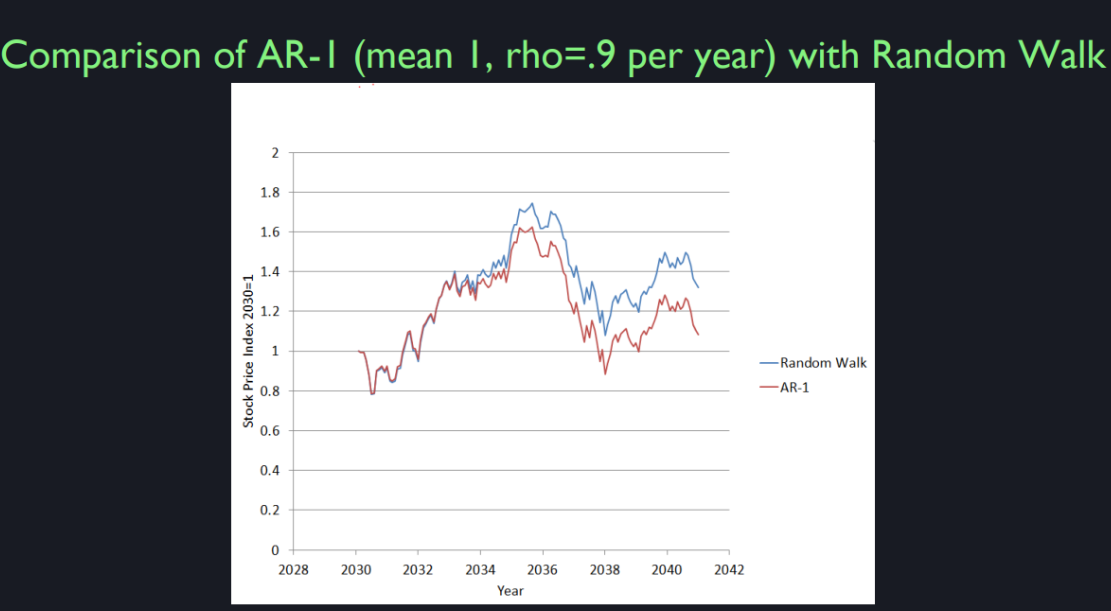

Now another alternative to a random walk,

a random walk has the property x sub t, if x is the random walk at time t,

is equal to its previous value plus noise epsilon sub t, and

the noise is totally unforecastable. An alternative to a random

walk model is a first-order autoregressive model, an AR-1 model. In this case, 100 represents the lamp

post, it’s the starting point. And then x sub t, the position at time t, is equal to the starting point +

rho where rho is between -1 and plus one, usually positive,

times xt -1- 100. So what this is, is a model which is modifying the drunk

at the lamp post a little bit. He’s now has a piece of elastic

wrapped around his ankle. And the elastic is tied to the lamp post. So if he starts walking away from

the lamp post in any direction, he gets tugged a little bit back to it. And the further away he goes,

the more he’s tugged back. So, in this case, this is xt-1-100 is how far

he is from the lamp post. And if rho is some high value, then, that means there isn’t that much of a tug,

that it’s a weak piece of elastic. So he can go wandering off, but

eventually, he’s going to come back. So this is mean reverting,

it’s reverting back to the lamp post.

Now the question is, there were a lot of studies suggesting

that the stock market is a random walk. But how do we know whether it’s

really a random walk or it’s an AR-1? Maybe when the stock market gets

really high, it’s going to go back. But not right away. But eventually, there’s something

tugging it back to a normal level. And when it gets really low,

it’s going to go back up. The problem is that it’s hard to

tell a distinction, if rho equals 1, you can see these hundreds drop out,

and it’s just a random walk. But if rho is lower than 1 but

not a whole lot lower than 1, then you really can’t tell whether

it’s a random walk or not. So this is an example of

a realization of a random walk, the blue line, and

an AR-1 with rho equals 0.9. And I defy you to tell me which one

of those is the, well, you can tell. In comparison,

this one started not at 100 but at 1, so you can see that the AR-1 it’s

come closer that’s the red line. It’s come closer back

to the starting point. The random walk has no tendency to

come back to the starting point. If stock prices are an AR-1, then it means

you should stay out of the market when the price is too high and

go back in when the price is too low. Which is different advice

than the random law theory.

Many would argue that when

you’re forecasting the future, whether economists or people in finance

who are working in Wall Street, for instance, forecasting what the future

of a market is going to look like, to look at what’s happened in recent

history, and try to project it forth. And using a rational, logic model-

Right. >> To try to project into the future. But, of course, you talk a lot about

sort of the irrational nature of the market and how we’re behavioral,

how we’re rational beings. But what I’m curious is, how do you

build in risk management to factor into sort of the irrational

nature of the markets and to capture sort of some of that irrational

exuberance that you talked about and the bubbles that might arise in

such things as housing markets?

Well, deep question, how do we handle? Why do we have irrational

exuberance at some times and not other times, and

what can we do about that [LAUGH]? Our principle to all that you talked

about is Central Bank policy. And Central Banks when they

think that the market is becoming overpriced, can tighten credit. And alternatively, when they think it’s

underpriced, they can loosen the credit. That is a tool that is being used. Although Central Banks don’t seem too

enthusiastic about trying to stabilize financial markets, it does seem to

influence their decision making. But that doesn’t get at

the basic psychology very much. So the problem is people are looking at the price of a speculative

asset as something largely separate from the underlying business that

is paying the bills, paying the dividends. They seem to often be looking

at the psychology of the market. They’re looking at trends

of technical analysis and they become unfocused on

the real fundamental which you might think ought to determine

the long run value of an investment. They’re focus is too much on the

short-term, predicting what it will do in the next month or so,

between the time I buy and sell. So there have been proposals

that might limit or reduce that short-term

speculative component.

So one idea is to put a transactions

tax on securities trades. So that would more force people to, or encourage them to be longer-term

in their investment. We have a distinct, that we have limited. We also have a capital gains tax that

distinguishes between short-term and long-term capital gains. And a reason to do that is to discourage

people from being short-term holders. They’ll end up paying

a capital gains tax on profit. There’s other longer term proposals. Mike O’Brennan at UCLA proposed that

we should create separate markets for corporate dividends at various horizons,

so that you’re focused on a dividend that some day in

the future you’re making an investment. You thought that would focus people

thinking on the fundamental. Well, now we do have markets for

claims and dividends that hasn’t

had any major impact. The problem is here that human

psychology is not easily managed. Talk to a psychiatrist and

you’ll hear that. We have antipsychotic drugs, they help,

but they don’t cure in a routine way. The same thing is true for anything you

might think of that might deal with irrational exuberance in the market. I wish we had lithium which is what

they use for irrational exuberance and bipolar disorder, but

it is not functioning in the stock market. >> Sure.

The key points of the professor’s talk can be summarized as follows:

Efficient Markets Hypothesis (EMH)

- Definition and History:

- EMH posits that market prices reflect all available information, making stock price movements unpredictable.

- An experiment with the S&P 500 index from 1950 to the present showed that most people’s predictions did not align with the random walk theory (an aspect of EMH).

Random Walk Theory

- Definition:

- Introduced by statistician Karl Pearson in 1905, it suggests that price changes are completely random and unpredictable.

- The analogy of a drunkard’s walk around a lamppost illustrates the random walk: predicting the drunkard’s future position means predicting the lamppost, as each step is random.

Autoregressive Model (AR-1 Model)

- Definition:

- An alternative to the random walk, assuming price changes are influenced by mean reversion.

- Prices deviate from the mean but gradually revert, though not immediately.

Behavioral Economics

- Representativeness Heuristic:

- People tend to predict future trends based on past patterns rather than adopting the random walk or mean reversion models.

Popularization of Random Walk Theory

- “A Random Walk Down Wall Street”:

- Burton Malkiel’s 1973 book advocates that stock prices follow a random walk and advises holding a diversified portfolio.

- Despite promoting EMH, Malkiel’s book includes some investment advice that doesn’t fully align with the theory.

Risk Management

- Market Psychology and Central Bank Policy:

- Central banks can tighten or loosen credit to address market overheating or cooling, but this doesn’t completely manage market psychology.

- Short-term speculative behavior is seen as a cause of market volatility and can be mitigated through measures like transaction taxes or differentiated capital gains taxes.

Conclusion

The professor discusses the history and theory of EMH, demonstrating the distinctions between the random walk theory and the autoregressive model, and analyzing the role of behavioral economics in market predictions. He also examines the role of central bank policies and market psychology in risk management, emphasizing the importance of reducing short-term speculation. Lastly, he notes the challenge of managing human psychology, making complete control over market fluctuations difficult.

教授的要点可以总结如下:

效率市场假说(Efficient Markets Hypothesis, EMH)

- 定义和历史:

- EMH主张市场价格反映所有可得信息,因此股票价格变动是不可预测的。

- 1950年代的标准普尔500指数预测实验显示,大多数人的预测并不符合EMH的随机漫步理论(random walk theory)。

随机漫步理论

- 定义:

- 由统计学家卡尔·皮尔森在1905年提出,认为价格变化是完全随机且不可预测的。

- 用醉汉在灯柱旁的行走来比喻随机漫步,预测醉汉的未来位置是灯柱,因为每一步的方向是随机的。

自回归模型(AR-1 Model)

- 定义:

- 是随机漫步的替代模型,假设价格变化受到平均回归(mean reverting)的影响。

- 价格偏离均值后会逐渐回归,但不会马上回归。

行为经济学

- 代表性启发法(Representativeness Heuristic):

- 人们倾向于用过去的模式预测未来,而不是采用随机漫步理论或平均回归模型。

随机漫步理论的普及

- 《漫步华尔街》:

- 伯顿·马尔基尔在1973年出版的书主张股市价格是随机漫步的,建议持有多样化的投资组合。

- 马尔基尔在书中仍然包含了一些与EMH不完全一致的投资建议。

风险管理

- 市场心理与中央银行政策:

- 中央银行可以通过紧缩或宽松信贷来应对市场过热或过冷,但难以完全管理市场心理。

- 短期投机行为被认为是导致市场波动的原因之一,可以通过交易税或资本利得税来减少。

总结

教授探讨了EMH的历史与理论,展示了随机漫步理论和自回归模型的区别,并分析了行为经济学在市场预测中的作用。他还讨论了市场心理和中央银行政策在风险管理中的角色,强调了减少短期投机的重要性。最后,他指出人类心理难以管理,因此市场波动难以完全控制。

Wall Street

华尔街简介

华尔街位于纽约市曼哈顿下城,是全球最重要的金融中心之一。它代表了美国的金融市场,并且是许多重要金融机构的所在地。以下是对华尔街的概述:

历史背景

- 起源:"华尔街"这个名字源于17世纪,当时荷兰定居者为了保护新阿姆斯特丹(现在的纽约市)免受英国和美洲原住民的攻击,修建了一道墙。这道墙就位于现在的华尔街位置。

- 发展:随着时间的推移,华尔街演变成了一个繁忙的商业和贸易中心。18世纪末,随着1792年《梧桐树协议》的签订和纽约证券交易所(NYSE)的成立,华尔街成为金融活动的核心。

金融机构和市场

- 纽约证券交易所(NYSE):位于华尔街11号,NYSE是全球市值最大的证券交易所,它在全球金融中扮演着重要角色。

- 纳斯达克(NASDAQ):尽管不在华尔街上,但纳斯达克通常与华尔街联系在一起。它是第二大证券交易所,并且以电子交易为主。

- 主要银行和公司:华尔街汇集了许多重要金融机构的总部和办公室,如高盛(Goldman Sachs)、摩根士丹利(Morgan Stanley)、摩根大通(JPMorgan Chase)、花旗集团(Citigroup)和美国银行美林(Bank of America Merrill Lynch)。

在全球金融中的作用

- 经济影响:作为全球金融中心,华尔街对世界市场有着重要影响。它吸引投资、促进贸易并推动经济政策。

- 金融服务:该地区提供广泛的金融服务,包括投资银行、资产管理、经纪和交易等。

文化和象征意义

- 美国资本主义的象征:华尔街代表了美国金融系统的力量和影响力,通常被用来指代整个金融部门。

- 文化参考:华尔街出现在许多电影、书籍和媒体中,往往象征着资本主义的繁荣与过度。术语“华尔街”有时被用来描述金融市场和大企业。

近期发展

- 技术进步:随着金融科技、电子交易和高频交易的兴起,华尔街不断适应并将先进技术融入其运作。

- 监管:2008年金融危机后,华尔街面临更多的监管审查,以防止未来的经济崩溃。像《多德-弗兰克法案》这样的改革旨在提高透明度并减少金融市场的风险。

结论

华尔街不仅仅是纽约市的一条街道,它是全球金融系统的中心,影响着经济,推动金融创新,并象征着现代资本主义的复杂性。

Wall Street is a significant financial district located in Lower Manhattan, New York City. It is synonymous with the American financial markets and is home to some of the most important financial institutions in the world. Here’s an overview:

Historical Background

- Origins: The name “Wall Street” originates from the 17th century when a wall was constructed by Dutch settlers to protect the New Amsterdam settlement from British and Native American attacks. The wall was located on what is now Wall Street.

- Development: Over time, Wall Street evolved into a bustling center for commerce and trade. By the late 18th century, it became the hub of financial activities with the establishment of the New York Stock Exchange (NYSE) in 1792 under the Buttonwood Agreement.

Financial Institutions and Markets

- New York Stock Exchange (NYSE): Located at 11 Wall Street, the NYSE is the largest stock exchange in the world by market capitalization of its listed companies. It plays a critical role in global finance.

- NASDAQ: Although not physically located on Wall Street, NASDAQ is often associated with it. It’s the second-largest stock exchange and operates electronically.

- Major Banks and Firms: Wall Street hosts the headquarters and offices of major financial institutions such as Goldman Sachs, Morgan Stanley, JPMorgan Chase, Citigroup, and Bank of America Merrill Lynch.

Role in Global Finance

- Economic Impact: Wall Street is a global financial hub that significantly influences world markets. It attracts investment, facilitates trade, and drives economic policies.

- Financial Services: The district offers a wide range of financial services, including investment banking, asset management, brokerage, and trading.

Cultural and Symbolic Significance

- Symbol of American Capitalism: Wall Street represents the power and influence of the U.S. financial system. It’s often used as a metonym for the financial sector as a whole.

- Cultural References: Wall Street has been featured in numerous films, books, and media, often symbolizing both the prosperity and the excesses of capitalism. The term “Wall Street” is sometimes used to describe financial markets and big businesses in general.

Recent Developments

- Technological Advances: With the rise of fintech, electronic trading, and high-frequency trading, Wall Street has adapted to incorporate advanced technologies into its operations.

- Regulations: Post-2008 financial crisis, Wall Street has seen increased regulatory scrutiny to prevent future economic collapses. Reforms like the Dodd-Frank Act aim to increase transparency and reduce risk in financial markets.

Conclusion

Wall Street is more than just a street in New York City; it is the epicenter of the global financial system, influencing economies, driving financial innovation, and symbolizing the complexities of modern capitalism.

Intuition of Efficiency

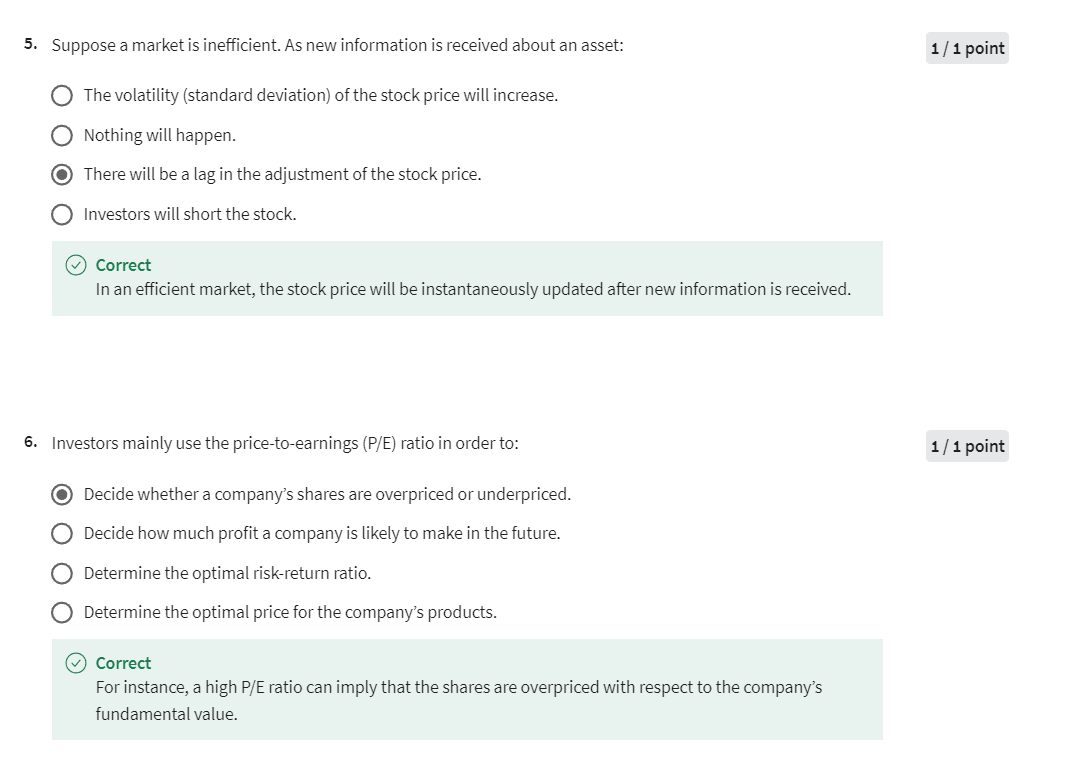

So let me just talk about what, I mean, I gave you history of thought, sort of about market efficiency. And and what people have thought over the time. Starting in the 19th century, information technology began to develop. There was a man named Reuter, who in just before the invention of the telegraph, decided that stock markets need up-to-date information. And so, he thought, how “How can I get information fair or of sell information?” So what he does is, these pigeons fly faster than any human transport, carrier pigeons. So what he did is he set up offices in major European cities and bought pigeons. And pigeons, and as soon as some market event happened in London, he would tie a piece of paper to the leg of the pigeon in London and send the news to Paris. And how long will it take a pigeon to fly from London to Paris? I don’t know. It takes 4-6 hours for a pigeon to fly from London to Paris. So it gave a trading advantage to people. So he was a big success with his pigeon service, and later, when they invented the telegraph. That that was here in New Haven, By the way way, Samuel F. B. Morse invented the telegraph. What year was that? Wasn’t it around 1840? I don’t remember exactly. The Reuter went to the telegraph to speed it up even more.

By the late 19th century, everyone was getting information with the speed of electricity. And they got beepers in the 20th century installed that would beep them when there were some important news. They would carry that around. Even before you had a cell phone, you could get a beeper. So the idea is that the information, there’s so many smart people trying to get information. It must be hard to beat the market and that means that you really can’t predict it. So the random work became plausible because people thought, “Yeah, all these people are trying so hard to get the information as quickly as they can and they trade on it as soon as they get it.” So doesn’t that mean that if anyone has some idea, so if the market goes down in London, it will probably go down in Paris too. So if the London market falls, you would like to sell in Paris. The problem is you can’t get the information in Paris fast enough. But now that they get it really fast. the market must adapt, adjust almost immediately. So this is what it came to.

The reason efficient market sounds plausible is you have to educate people out of naive ideas that they can predict the market. So some people will go to their broker and say, “You know, the other day I read in the Wall Street Journal that this company has a new drug that’s about to come out, so is that a reason for me to buy?” Then, the broker will tell you, “You read it when, last week?”. Your broker might say, “When that news came out, I remember my beeper went off immediately and I rushed to my colleagues and said, what’s this news mean?” And someone said, “Sell, sell right now.” So I placed an order in 15 seconds. He had it and said, “You got to beat the others.” And then I said, “I just saw but I hadn’t even had 15 seconds to talk about it.” They talked more about it and they think, “Well, maybe I shouldn’t have sold.” So 30 seconds later, you buy. And then within two minutes, they’ve got got an expert advice on what it means and the market has gone wild, and now it sells down at the new optimal level. So, maybe the market wasn’t perfectly efficient for 15 seconds. But you had better be educated that if you read something in the newspaper last week week, it’s already incorporated into in the market prices. Even in 1889, it oh, I didn’t have beepers then.

A moment’s reflection should convince that person that a function which occupies so important a place in the mechanism of modern business must be a useful and necessary part of the economy片刻的思考应该使那个人相信,在现代商业机制中占有如此重要地位的一项职能一定是经济中有用和必要的一部分

Here’s a 1904 article, it’s a really nice article by Charles Conant. In in a magazine, and it’s about the beauty of markets, and he was referring to the public. He referred to a ignorant public view that markets are a sort of gambling casino. But he said, a “A moment’s reflection should convince that person that a function which occupies so important a place in the mechanism of modern business must be a useful and necessary part of the economy.” Yeah, what he’s getting at is that those prices in markets are the result of people trying to figure out values, and if we didn’t have the markets, we wouldn’t know what anything was worth. Any business plan involves prices. As a business, you’re going to have to buy commodities or you’re going to have to borrow at interest rate. All these prices are relevant to an intelligent decision. So not only are markets efficient in the current economy, they’re better knowledge than any individual because it involves so many people of all putting their money on the line and trading them. And then it produces values which he implicitly assumes in 1904, are the best estimate of fundamental value, and then it drives businesses and make decisions, whether to build a new factory or to hire new people based on these prices. So it’s a beautiful system that he talks about. Until the financial crisis.

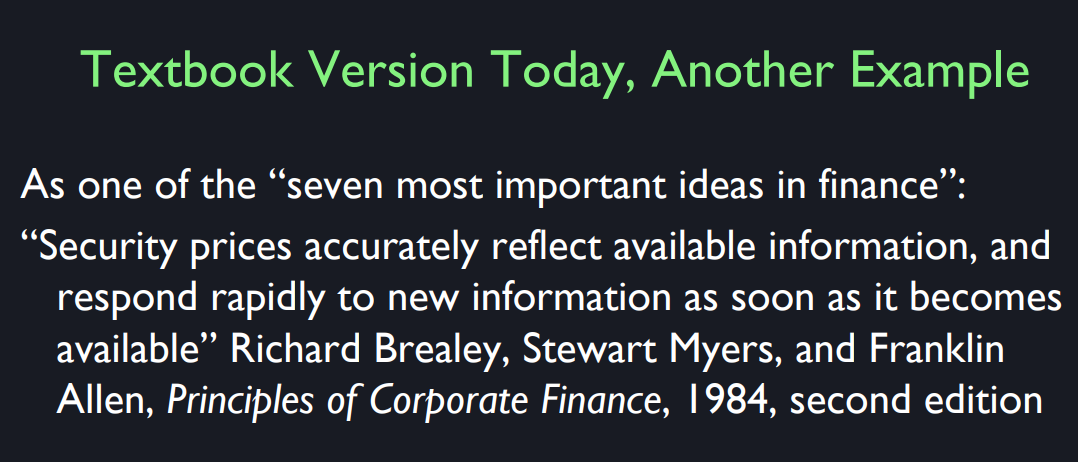

Textbooks were glowing in defense of the financial market. Even your textbook Fabozzi those in an earlier edition in 2002 said, “Publicly available, relevant information will lead to correct pricing of freely traded securities in properly functioning markets.” Here’s another textbook of finance by Richard Brealey and Stewart Myers in an earlier edition.

Security prices accurately reflect the available information, and respond rapidly to new information as soon as it becomes available 证券价格准确地反映了可获得的信息,并在新信息出现时迅速作出反应

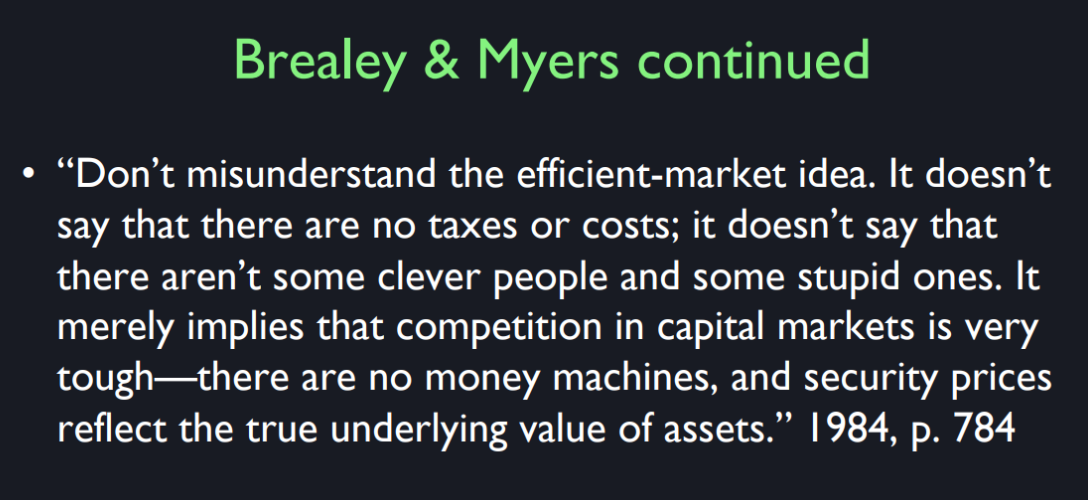

Efficient markets really took hold the theory in people’s thinking, starting after [inaudible] book. It really was intellectual revolution. But according to Brealey, Myers and Allen. “Security prices accurately reflect the available information, and respond rapidly to new information as soon as it becomes available.” That’s a pretty strong statement, and then they did qualify it. “Don’t misunderstand the efficient markets idea. It doesn’t say that there are no taxes or costs. It doesn’t say that there aren’t some clever people and some stupid ones. It merely implies that competition in capital markets is very tough. There are no money machine, and security prices reflect the true underlying value of assets.” So he’s not really qualified. They’re not really qualifying it very much. They’re telling you to believe prices you see in the markets as if they were truth.

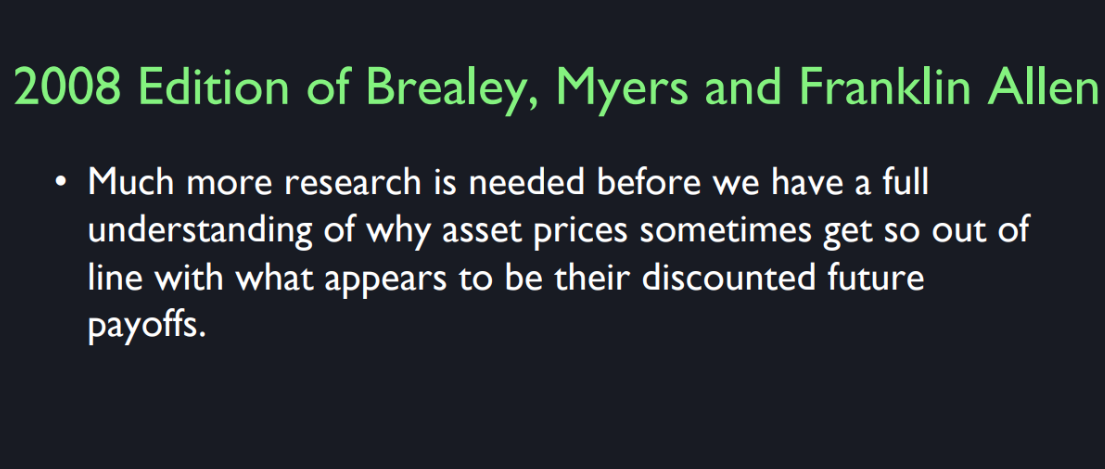

They have subsequently however, in their 2000 a day eighth edition edition, this is after the beginning of the financial crisis. They have qualified it. I don’t mean to laugh. They’re great people. They’re reflecting, when you read a textbook, the ideas of the time. But I’m just using this as a sign of how much. Thinking has changed. They now say say, “Much more research is needed before we have a full understanding of why asset prices sometimes get so out of line with what appears to be their discounted future payoffs.”

Much more research is needed before we have a full understanding of why asset prices sometimes get so out of line with what appears to be their discounted future payoffs 在我们完全理解为什么资产价格有时会如此偏离其贴现的未来收益之前,还需要进行更多的研究

So the efficient markets hypothesis has taken a hit after the financial crisis, and you can see it in the textbooks. So, I think efficient markets is like that it was a scientific revolution that came out really in the '60s, and then the '70s, and it led to the extreme bull market that we had around the world in the 1990’s. People then finally decided that whatever the stock market does is right. Whatever the housing market does is right because its markets are efficient, and that unfortunately wasn’t quite right.

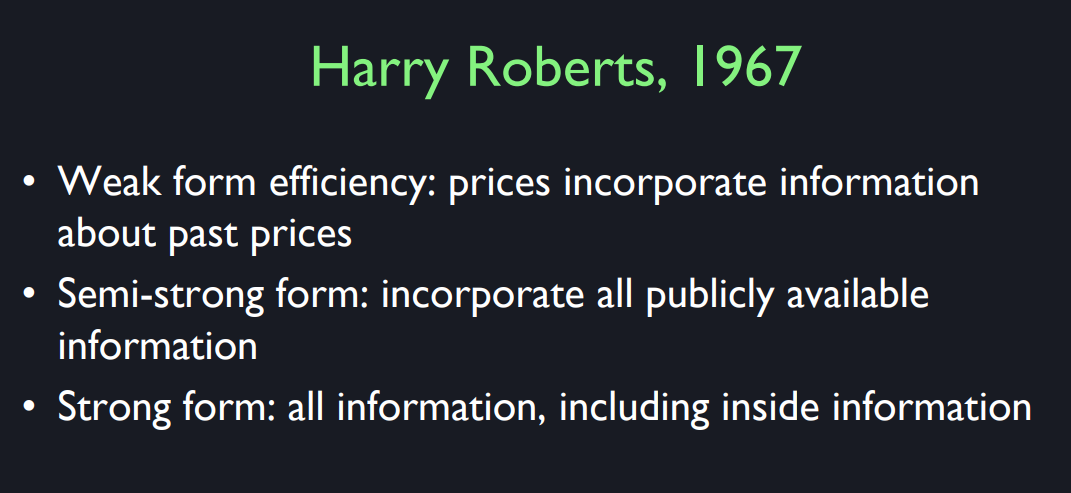

Harry Roberts is the coiner of the term efficient markets. Although I’ve traced the history back almost 100 years before him they didn’t call it the efficient markets hypothesis. He said there are three forms for market efficiency. Weak form is that information in past prices can’t help you to forecast, the semi-strong form of efficient markets is that all publicly information is already incorporated in the market prices, and the strong form is that all information including inside information held by the companies is already incorporated in the stock prices, prices because it leaks out. Companies can’t keep secrets. Actually, I think this semi-strong form is the one that we focus on. I don’t think that companies can’t keep secrets. They sometimes leak out but they don’t always leak out.

哈里·罗伯茨(Harry Roberts)提出了市场有效性(Efficient Markets)的概念,并将市场有效性分为三种形式:弱式有效市场、半强式有效市场和强式有效市场。这三种形式描述了市场价格反映信息的程度。以下是对每种形式的介绍:

- 弱式有效市场

- 定义:在弱式有效市场中,市场价格已经反映了所有历史价格和交易量数据。这意味着过去的交易信息已经被纳入当前的股票价格中。

- 含义:技术分析(依赖于过去价格走势来预测未来价格)无法持续获得超额收益,因为过去价格中的任何信息都已经反映在当前价格中。

- 例子:如果某只股票在过去一个月内价格持续上涨,弱式有效市场认为,仅凭这个趋势无法可靠地预测未来的价格走势。

- 半强式有效市场