第一次发说有广告嫌疑,有编辑一次,尽可能去除广告内容。

Python股票量化投资课学习—小市值策略测试

测试平台—

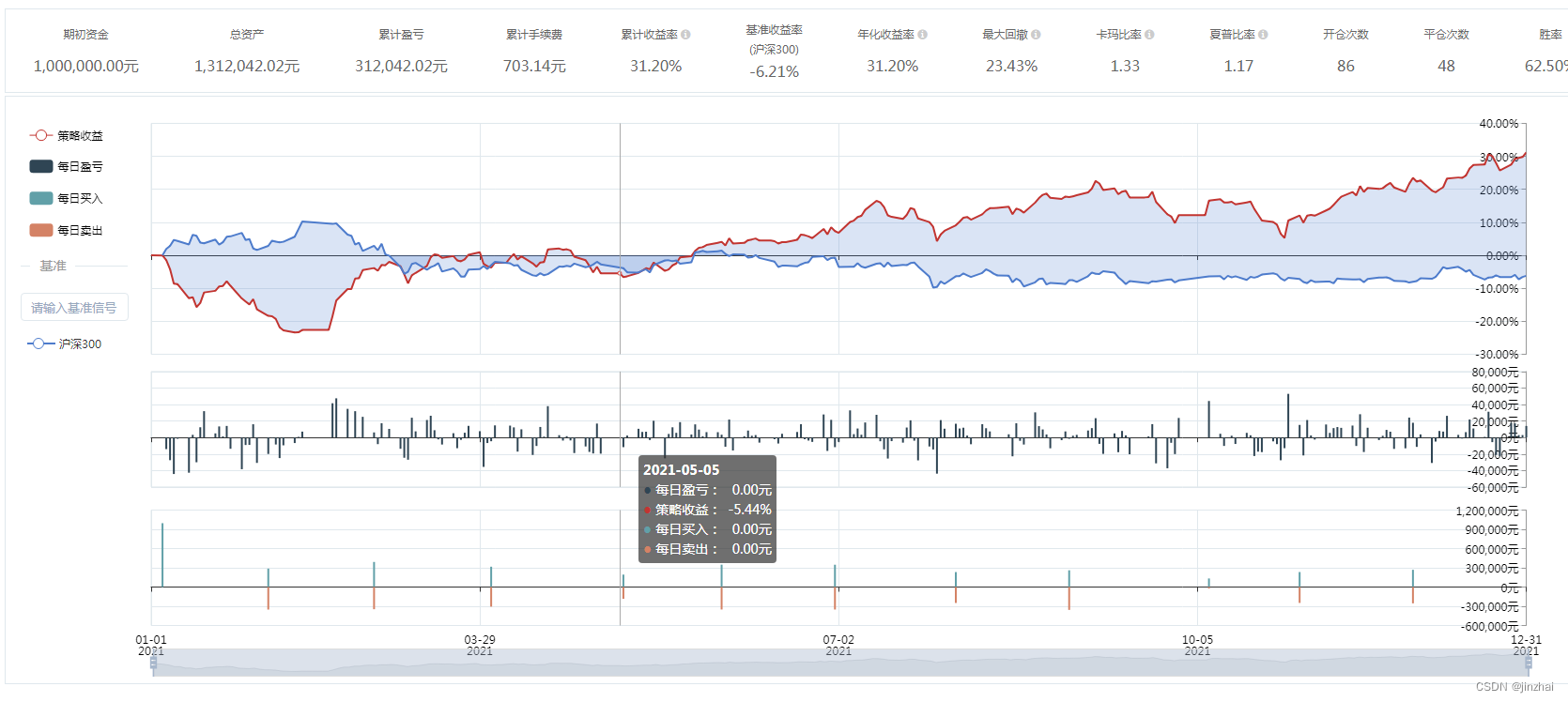

小市值策略测试 测试结果如下:

小市值策略测试 思路如下:

选股策略:市值因子

具体内容:在没个月的最后一个交易日,将所有股票按照市值从小到大排序,买入市值最小的10只股票。持有接下来的一个月,到下个月底的时候,按照同样的规则,买入另外10只股票,如此往复。

小市值策略测试 测试源文件如下:

源文件下载地址:https://download.csdn.net/download/jinzhai/86402507

小市值策略测试 源码如下:

# coding=utf-8

from __future__ import print_function, absolute_import, unicode_literals

from gm.api import *

import datetime

"""

示例策略仅供参考,不建议直接实盘使用。

小市值策略,等权买入全A市场中市值最小的前N只股票,月初调仓换股

"""

def init(context):

# 定时任务,月频(仿真和实盘时不支持该频率)

schedule(schedule_func=algo, date_rule='1m', time_rule='09:31:00')

# 定义股票池数量

context.num = 10

def algo(context):

# 当前时间

now = context.now

# 上一交易日

last_date = get_previous_trading_date(exchange='SZSE', date=now)

# 获取A股代码(剔除停牌股、ST股、次新股(365天))

all_stock,all_stock_str = get_normal_stocks(now)

# 获取所有股票市值,并按升序排序

fundamental = get_fundamentals_n('trading_derivative_indicator', all_stock_str, last_date, fields='TOTMKTCAP', count=1, df=True).sort_values(by='TOTMKTCAP')

# 获取前N只股票

to_buy = list(fundamental.iloc[:context.num,:]['symbol'])

print('本次股票池有股票数目: ', len(to_buy))

positions = context.account().positions()

# 平不在标的池的股票

for position in positions:

symbol = position['symbol']

if symbol not in to_buy:

order_target_percent(symbol=symbol, percent=0, order_type=OrderType_Market,position_side=PositionSide_Long)

# 获取股票的权重

percent = 1 / len(to_buy)

# 买在标的池中的股票

for symbol in to_buy:

order_target_percent(symbol=symbol, percent=percent, order_type=OrderType_Market,position_side=PositionSide_Long)

def on_order_status(context, order):

# 标的代码

symbol = order['symbol']

# 委托价格

price = order['price']

# 委托数量

volume = order['volume']

# 目标仓位

target_percent = order['target_percent']

# 查看下单后的委托状态,等于3代表委托全部成交

status = order['status']

# 买卖方向,1为买入,2为卖出

side = order['side']

# 开平仓类型,1为开仓,2为平仓

effect = order['position_effect']

# 委托类型,1为限价委托,2为市价委托

order_type = order['order_type']

if status == 3:

if effect == 1:

if side == 1:

side_effect = '开多仓'

elif side == 2:

side_effect = '开空仓'

else:

if side == 1:

side_effect = '平空仓'

elif side == 2:

side_effect = '平多仓'

order_type_word = '限价' if order_type==1 else '市价'

print('{}:标的:{},操作:以{}{},委托价格:{},委托数量:{}'.format(context.now,symbol,order_type_word,side_effect,price,volume))

def get_normal_stocks(date,new_days=365):

"""

获取目标日期date的A股代码(剔除停牌股、ST股、次新股(365天))

:param date:目标日期

:param new_days:新股上市天数,默认为365天

"""

if isinstance(date,str) and len(date)==10:

date = datetime.datetime.strptime(date,"%Y-%m-%d")

elif isinstance(date,str) and len(date)>10:

date = datetime.datetime.strptime(date,"%Y-%m-%d %H:%M:%S")

# 先剔除退市股、次新股和B股

df_code = get_instrumentinfos(sec_types=SEC_TYPE_STOCK, fields='symbol, listed_date, delisted_date', df=True)

all_stocks = [code for code in df_code[(df_code['listed_date']<=date-datetime.timedelta(days=new_days))&(df_code['delisted_date']>date)].symbol.to_list() if code[:6]!='SHSE.9' and code[:6]!='SZSE.2']

# 再剔除当前的停牌股和ST股

history_ins = get_history_instruments(symbols=all_stocks, start_date=date, end_date=date, fields='symbol,sec_level, is_suspended', df=True)

all_stocks = list(history_ins[(history_ins['sec_level']==1) & (history_ins['is_suspended']==0)]['symbol'])

all_stocks_str = ','.join(all_stocks)

return all_stocks,all_stocks_str

def on_backtest_finished(context, indicator):

print('*'*50)

print('回测已完成,请通过右上角“回测历史”功能查询详情。')

if __name__ == '__main__':

'''

strategy_id策略ID,由系统生成

filename文件名,请与本文件名保持一致

mode实时模式:MODE_LIVE回测模式:MODE_BACKTEST

token绑定计算机的ID,可在系统设置-密钥管理中生成

backtest_start_time回测开始时间

backtest_end_time回测结束时间

backtest_adjust股票复权方式不复权:ADJUST_NONE前复权:ADJUST_PREV后复权:ADJUST_POST

backtest_initial_cash回测初始资金

backtest_commission_ratio回测佣金比例

backtest_slippage_ratio回测滑点比例

'''

run(strategy_id='strategy_id',

filename='main.py',

mode=MODE_BACKTEST,

token='{{token}}',

backtest_start_time='2021-01-01 08:00:00',

backtest_end_time='2021-12-31 16:00:00',

backtest_adjust=ADJUST_PREV,

backtest_initial_cash=1000000,

backtest_commission_ratio=0.0001,

backtest_slippage_ratio=0.0001)